A farmer seeding new lines of Kapphaphycus striatus in the island of Guindacpan, Northern Bohol in the Philippines © Karlotta Rieve, Hatch Innovation Services

There is no shortage of good news stories about the potential of seaweed farming. From ecosystem services such as carbon sequestration, bioremediation and methane reduction, to the displacement of fossil fuels in hard-to-abate sectors such as construction or plastics, the potential benefits of farming seaweed are vast. They are also magnified by the socio-economic advantages of developing an industry that benefits coastal communities, often with strong female engagement.

Based on these benefits, the number of startups developing novel products and applications from seaweed in Europe and North America, has increased in recent years. This has been coupled with increasing investor interest in seaweed startups. In 2022, hundreds of millions of dollars were allocated to teams working primarily on biorefineries, bioplastics, and methane reduction supplements.

Unfortunately, a recurring challenge relates to the patchy supply of seaweed. In developing seaweed regions like Europe and North America, there’s a "chicken and egg" problem, whereby buyers need a steady supply of seaweed for their processing facilities, while suppliers need proof that scaling will be met with adequate demand for their seaweed. This is often said to be the main barrier to growing the industry in the Western world.

This leads naturally to the questions: Where can supply for new and emerging seaweed-based products come from and where should investors deploy capital next?

Many farmers lack boats and farming materials that would make it possible to farm in deeper waters – making it more difficult to expand their farms, Rote Island, NTT, Indonesia © Karlotta Rieve, Hatch Innovation Services

A snapshot of the global seaweed sector

To date, over 12,000 species of seaweed are known. These are classified into three main types:

- Red seaweed (Rhodophyta), make up 52 percent of global seaweed supply and the main commercial red seaweed species contain carageenan and agar – both binding agents used in the food industry.

- Brown seaweed (Phaeophyceae), account for 47 percent of global production and are often rich in alginates. The larger species are often referred to as kelp.

- Green seaweed (Chlorophyta) are less commonly farmed and mostly found in shallow and intertidal areas.

However, only 0.1 percent of these species are commercially farmed today.

95 percent of global macroalgae production comes from five species groups; Saccharina, Eucheumatoids, Gracilaria, Pyropia and Undaria, based on 2020 figures provided by the Food and Agriculture Organization of the United Nations (FAO). This consolidation has taken place in the past two decades. Prior to that the contribution of other species was substantially higher.

The supply from traditional seaweed regions is slowing down

Commercial farming of seaweed began in Asia more than 50 years ago and has since grown rapidly. Although seaweed farms are starting to become popular in other parts of the world, Asian producers still dominate the seaweed market – both in terms of volume and value – with over 95 percent of the market share in 2020. The largest producers are China and Indonesia, which supply 56 percent and 27 percent of farmed seaweed respectively, followed by South Korea.

Countries outside of Asia produced less than 2 percent of the total farmed seaweed volumes in 2020. Tanzania (in particular Zanzibar) and Chile are the next two most productive regions outside of Asia, accounting for 0.3 percent and 0.1 percent respectively of the world’s seaweed aquaculture production.

Total collapse of Saccharina production in 2022 from China

Blades of Saccharina japonica can grow up to 8 metres over the winter months and become so heavy that farmers have to use cranes to lift the lines © Karlotta Rieve, Hatch Innovation Services

Although China’s production figures were increasing until 2020, recent reports show that the country’s primary seaweed crop, Saccharina, has had poor harvests, which have decreased overall production significantly.

In Japan, production volumes for Saccharina have been decreasing since 1991 and Undaria have been decreasing as early as 1973.

South Korea’s seaweed production across the main species, Saccharina, Undaria and Pyropia, has been stagnating since 2017.

There are three main challenges for commercial cultivation of temperate seaweed species:

- Climate change is creating shorter seasons and warmer waters that cause a decrease in yields.

- Many of the major farming regions have reached maximum carrying capacity in the nearshore areas where the cultivation takes place.

- Labour costs are increasing and the seaweed farming workforce is aging.

Harvesting Undaria pinnatifida that will be fed fresh to abalone with cage culture in the background © Karlotta Rieve, Hatch Innovation Services

Tropical red seaweed volumes are much lower than official statistics

In terms of tropical seaweed production in Southeast Asia, Indonesia is the largest producer of Eucheumatoids as well as Gracilaria. Production volumes of Eucheumatoids in the Philippines and Malaysia have been decreasing since 2011 and 2012 respectively, according to the FAO dataset. This dataset is based on the reports of government agencies by producing countries, but our recent in-field work in this region revealed that the real production volumes are much lower.

According to government statistics, production in Indonesia increased nearly ten-fold between 2000 and 2015 but has been slightly decreasing/stagnating since, with a production of 7 million tonnes wet weight in 2021. However, according to several industry sources the realistic production volumes for Eucheumatoids in Indonesia may only be one sixth of the official figure. Similarly, the official Eucheumatoid volumes for the Philippines and Malaysia, as well as Gracilaria in Indonesia, don’t match with the actual production on the ground.

Although it seems that Indonesian seaweed aquaculture still has strong potential to expand, the sector’s development will be highly dependent on future demand. Meanwhile, it is unlikely that production in the Philippines or Malaysia will increase significantly in the near future.

There are three main challenges for the commercial cultivation of tropical seaweed species:

- The lack of quality seed supply – reduces yields and makes the crop more vulnerable to diseases and epiphytes.

- Climate change – is creating more extreme weather conditions and events more frequently that cause slow growth, cause diseases, increase epiphytes or can even destroy entire farm sites.

- Limited access to capital – is limiting opportunities for farmers to expand, rebuild farm sites, or source seed after severe weather events.

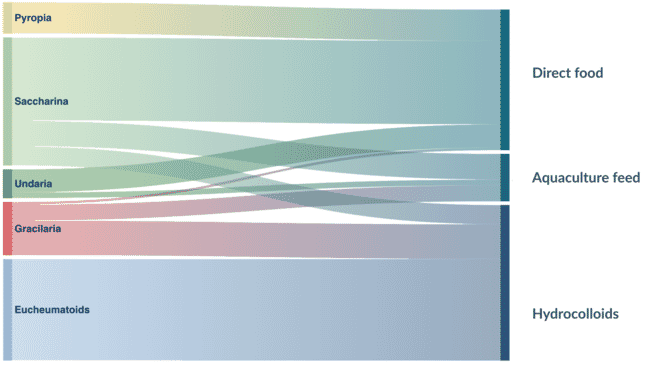

Current markets are soaking up most supply

Disclaimer: This is just on the basis of the field insights – therefore only data from the six countries studied – which account for 98 percent of global farmed seaweed according to FAO 2020 data © Hatch Innovation Services

Most farmed temperate seaweed species are destined for direct human consumption – in products including soups, snacks, flavoured sheets and fresh salads. They are mainly farmed and consumed in East Asia, and the demand – especially in China – has increased with the rise of e-commerce.

Meanwhile, much of the Undaria and Saccharina produced in South Korea and China is sold as live feed for the abalone aquaculture sector.

Seaweeds also provide hydrocolloids – such as agar, carrageenan and alginate – which are primarily used in the food industry for gelling, thickening, stabilising and emulsifying agents and are widely traded as commodities.

Carrageenan and agar are the primary reasons Eucheumatoids and Gracilaria farming in the Coral Triangle region was established. Today, these farmed seaweeds almost exclusively rely on hydrocolloid markets. The current supply chains are set up to almost exclusively cater the production of carrageenan or agar and trade networks are often complex and strongly dominated by Chinese conglomerates. Western companies looking to source red seaweed from the Coral Triangle region therefore have a hard time accessing supplies of raw materials. Hydrocolloid supply chains are often closely knit and difficult to access without having a physical presence in the country and established networks in the local seaweed sector.

2022 was an interesting year for these markets, as the prices for raw dried seaweed varied dramatically. As an example, in Indonesia the average farm gate price of cottonii, the most sought-after Eucheumatoid seaweed, fluctuated between $1,250 and $2,700 per dry tonne.

The price increases are due to supply chain disruptions caused by Covid-19 and the resulting speculation by big traders who were storing huge quantities of processed hydrocolloids for a long time, as well as the production downturn caused by global warming and disease.

The strong price increase is a complex phenomenon, with little data available, but – under normal market conditions – it would imply that the supply is not meeting demand. Despite this, the hydrocolloid industry is still increasing its processing capacities, with many investments being made directly in new processing facilities in Indonesia for alkaline treated chips and semi-refined carrageenan, which is further used to produce refined carrageenan abroad. The mismatch between processing capacities and raw material (seaweed) volumes is increasing the pressure on supply and leading to increased price volatility. Which, in turn, makes it difficult for newcomers in the seaweed processing space to purchase raw material for novel product applications.

When will seaweed production in new geographies scale?

Interest in seaweed production in other regions is growing, but these regions are not yet producing significant volumes.

The FAO data on production volumes in the rest of the world show stagnant or slowly increasing production only. Nevertheless, the public and private sectors in Europe, USA, Australia and New Zealand have made strong commitments to develop their seaweed industries and some pioneering farms show early traction. Similarly, many countries in Africa and Latin America have potential to leverage their long coastlines and Exclusive Economic Zones.

Interest in developing an industrial seaweed farming sector outside Asia is quite young. While more technologically advanced production systems have been developed in Northern Europe and North America, the growth rates of front runners like Alaska, Maine, France and Norway are conservative compared to the Asian first movers back in the 1970s.

A good example here is kelp production in Japan, the birthplace of Saccharina farming 50 years ago. Despite both countries having a temperate climate, concentrating on growing kelp species and having almost the same length of coastline available it seems unlikely that Norway will be able to emulate the stratospheric growth rate that Japan achieved.

Indeed Saccharina production in Japan increased almost 8,000 percent in only six years and 25,000 percent within 20 years. Given that Norway produced 248 tonnes in 2020 (similar to Japan’s 282 tonnes in 1970), to match Japan’s growth rate it would have to be producing 19,840 tonnes by 2026 and 62,000 tonnes by 2040.

While this might be feasible, it is clear that the circumstances for scaling seaweed production in Asia in the 1970s were different from conditions in the West today. Regulations, marine use conflict, the cost and availability of labour and seed material and high initial investment are some of the significant challenges facing Western producers. These factors were less prevalent in Asia during the 1970s.

The three way "chicken and egg problem" inhibiting leap of the Western seaweed sector

As most of the world’s seaweed startups are based in Europe and North America, the majority of venture capital investments in the sector are currently being made in these regions. And the majority of these investments are focusing on product development – the market side of things. Still, only a few hundred tonnes are currently being produced in Europe and North America, while other geographies are only slowly coming online.

However, many companies working on new product development for bioplastic, fabrics, pet or animal feed products for example, would need seaweed biomass inputs in the thousands of tonnes scale for commercial roll out. From our recent market study, where we spoke to many of them, we learned that they are struggling to source these raw materials locally and – given the physical and cultural distance to existing seaweed producing geographies – they are struggling to tap into existing Asian supply chains.

In theory, the cost of production for seaweed farming in the West – which are currently orders of magnitude higher than in Asia – should naturally come down once scaling effects kick in. However at the current price level and volumes of seaweed available in these geographies, hardly any new markets can develop to create the necessary demand for scaling.

Some suggest that by developing seaweed-based products with higher market values, such as nutraceuticals and pharmaceuticals, the resulting high production costs for seaweed can be compensated. Yet these applications have very long development cycles and would only need small quantities, which would not boost demand for farmed seaweed in volumes any time soon. Developing biorefineries seems the most promising route for a feasible seaweed sector in the West, at this point.

Such a way of processing would combine low volume/high value with high volume/low value products and therefore improve the business case for seaweed based products, where production costs are currently to allow for competitive outputs.

The only thing is that such processing facilities would require large scale investments, which at current scale of seaweed supply are certainly high risk and not attractive to private sector investors.

The public sector could play a role here by incentivising production with low cost, long term financing or incentivising legislation while production is scaling up. Subsidies that can help bridge the large gap between the cost of farmed seaweed and a reasonable input price that allows for the development of competitive products and applications from seaweed biomass.

Quality over quantity is the key to Saccharina japonica production for human consumption in South Korea, Japan and China © Karlotta Rieve, Hatch Innovation Services

The need for investment in primary production

As it stands now, the total amount of farmed seaweed across all geographies needs to increase from its existing baseline to allow the industry to boost the share of seaweed products across global markets.

Lessons can be learned from established seaweed regions, but development is needed, in both old and new regions, for the following:

- Breeding programmes to ensure high quality seed material

- Diversification of species

- Nursery efficiency

- Offshore technologies, monitoring and automation of farm processes

- Capacity building using best practices

- Legislation (Marine Spatial Planning)

- Access to capital

Conclusions

Our extensive research suggests that investors are potentially being misled by inaccurate seaweed production figures. Investing in primary production – be it establishing new farms or making existing ones more productive and efficient – might be the best way to catalyse the growth of the seaweed sector.

In Asia it is clear that the demand for raw seaweed is outstripping supply, generating excellent – albeit fluctuating – prices for efficient growers. Meanwhile, in the West, the paucity of production is preventing a growing number of startups from commercialising the products that they’ve been working hard to develop.

We hope that farmers, investors and regulators will take note of these bottlenecks in the supply chain and watch out for our more in-depth reports on these issues which are due out in the coming weeks. These will help to paint a fuller picture of a sector that has considerable long-term growth potential.

For additional data on the global macroalgae sector, visit Seaweed Insights.