Higher Yields Boost Corn Crop

Corn planted and harvested area are both reduced this month, but a 2.3-bushel-per-acre increase in yield raises forecast corn production 64 million bushels. Production is also increased for barley and oats, but lowered for sorghum. Feed grain production is expected to be the second highest ever. Corn feed and residual use is raised because of increased supplies. US corn exports are reduced mostly due to reduced demand prospects from Canada. World supplies and use of coarse grains are both increased this month, leaving global stocks nearly unchanged. Corn and sorghum prices are unchanged this month, but projected ranges for barley and oats are narrowed.

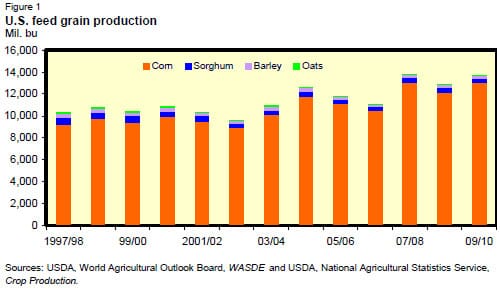

Feed Grain Production Up in 2009/10

US feed grain production for 2009/10 is forecast at 346.2 million tons, up from 344.8 million last month. The month-to-month increase reflects additions in corn, barley, and oats production but a reduction in sorghum production. Planted area for the four grains is decreased 900,000 acres, and harvested for grain acres were decreased 1.0 million acres this month. Yields per harvested acre for the four grains combined are increased slightly to 3.87 metric tons per acre, compared with 3.81 metric tons last month. Beginning stocks in 2009/10 are lowered slightly to 47.1 million tons. Total 2009/10 feed grain supply is forecast at 395.8 million tons, up from 394.6 million last month and up from 373.9 million in 2008/09.

Total 2009/10 feed grain utilization is projected at 348.6 million tons, down from 349.0 million last month, but up from 326.9 million in 2008/09. The month-tomonth decrease came from lower corn exports, and lower sorghum and barley feed and residual use. Total projected feed grain ending stocks for 2009/10 are raised 1.6 million tons to 47.2 million.

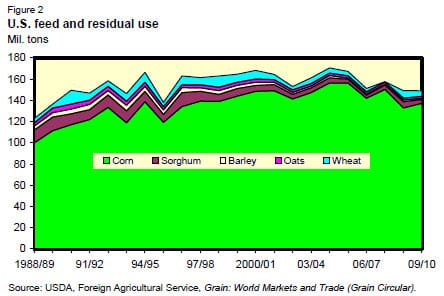

On a September-August marketing year basis for 2009/10, feed and residual use for the four feed grains plus feed wheat is projected to total 149.3 million tons, up from 144.9 in 2008/09. Corn is estimated to account for 92 per cent of feed and residual use in 2009/10. The projected index of grain-consuming animal units (GCAU) in 2009/10 is up 0.2 million units from last month to 91.3 million, but down from 92.8 million in 2008/09. Feed and residual per GCAU in 2009/10 is estimated at 1.63 tons, up from 1.56 tons in 2008/09.

Higher month-to-month feed and residual use reflects increases for corn as sorghum and barley feeding is lowered. Residual use is also expected to be higher for corn as this month’s corn yield forecast boosts 2009/10 supplies. Statistical analysis suggests that feed and residual use increases, when corn yields are above trend, even when other factors are unchanged. This month’s higher corn yield forecast suggests a larger residual, even though actual residual is never known. Feed needs for all the livestock classes are down from 2008/09 because producers are reducing livestock numbers as measured by GCAU. Cattle on feed GCAUs in 2009/10 are down 694,000 units from last year. In the September Cattle on Feed report, cattle numbers were down 1 per cent from last year and marketings of fed cattle were the lowest on record for August. Slow marketings usually mean heavier cattle consuming more feed, and indeed, slaughter weights were up in September.

Milk producers have been selling dairy cows to try to cut milk production and increase prices. Dairy GCAUs are down 333,000 from last year, suggesting lower feed needs, but milk per cow continues to rise and increase feed needs.

The Quarterly Hogs and Pigs report, released 25 September, indicated that producers plan to farrow fewer sows during the remainder of 2009 and into 2010, which, coupled with fewer imports of hogs from Canada, results in a lower production forecast. The lower pork production reduced pork GCAUs and suggests feed needs should be lower. Poultry GCAUs are also down from last year but less than the red meats. Livestock and poultry producers are struggling with weak demand for their products, and large supplies of meat and high feed costs continue to pressure prices.

Minor Changes Made to 2008/09 Crop Year

The following changes were made to the 2008/09 balance sheets:

- Corn: imports were lowered 1 million bushels to 14 million; feed and residual use was lowered from 5,250 million bushels to 5,231 million; feed, seed and industrial use was raised 31 million bushels to 4,976 million bushels, with most of the increase in corn used for ethanol; exports were raised 8 million bushels to 1,858 million bushels; ending stocks were lowered from 1,695 million bushels to 1,674 million; and, prices per bushel were lowered from $4.08 to $4.06.

- Sorghum: feed and residual use was raised 2 million bushels to 232 million; food, seed and industrial use was lowered 15 million bushels to 95 million; exports were lowered 2 million bushels to 143 million; ending stocks were raised 15 million bushel to 55 million; and prices per were lowered from $3.23 to $3.20.

- Barley: production was raised from 239 million bushels to 240 million; and feed and residual use was raised 0.5 million bushels to 67 million.

- Oats: yield was raised 0.2 bushels per acre to 63.7 bushels, as a result production was increased slightly; feed and residual use was raised 1.0 million bushels.

2009/10 Corn Crop Forecast as Second Largest

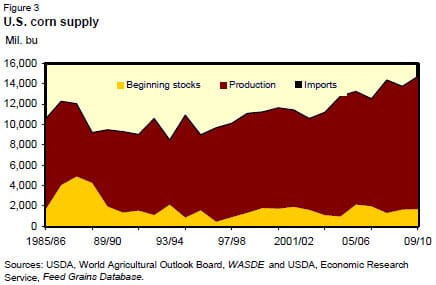

Corn production is forecast at 13,018 million bushels, up 64 million from last month and up from 12,101 million in 2008/09. The forecast was raised because of increased yields, up 2.3 bushels per acre from last month and up from 153.9 bushels per acre last year. If realized, this yield will be the highest on record. Based on administrative data, corn planted and harvested area were each reduced 700,000 acres. States with the largest decreases in planted and harvested acreage are Illinois (300,000 acres), Nebraska (250,000 acres), Indiana, Michigan, Minnesota, and Missouri (100,000 acres each). Beginning stocks were lowered to 1,674 million bushels, and total supply is projected at 14,702 million bushels, up from 13,739 million a year earlier.

The 1 October corn objective yield data indicate a record-high number of stalks and ears per acre for the combined 10 objective yield States (Illinois, Indiana, Iowa, Kansas, Minnesota, Missouri, Nebraska, Ohio, South Dakota, and Wisconsin). All objective yield States, except Missouri, recorded record high ear counts.

On the use side, feed and residual use was raised 50 million bushels to 5,400 million because of the potential for more residual, with the forecast yield well above trend. Corn used for ethanol production in 2009/10 was unchanged this month, even though ethanol production in July (latest numbers available) was 948 million gallons, a new record. Weekly gasoline blended with alcohol was rising in June, July, and August, but in September turned down sharply bring into question whether gasoline demand will support expanded ethanol production. Corn used for high fructose corn syrup (HFCS) was increased 5 million bushels this month because of tightening supplies of sugar. Exports are projected 50 million bushels lower on reduced demand from Canada. Total utilization is projected at a record 13,030 million bushels, up 5 million from last month, and up 965 million from 2008/09.

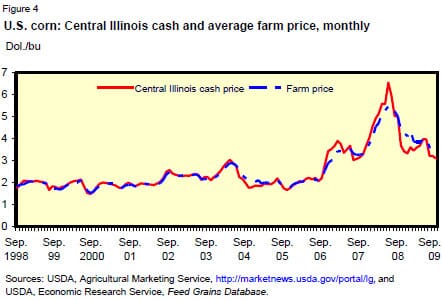

Ending stocks were raised this month by 37 million bushels to 1,672 million bushels. Prices received by farmers are expected to range between $3.05 and $3.65 per bushel, unchanged from last month and compared with $4.06 in 2008/09.

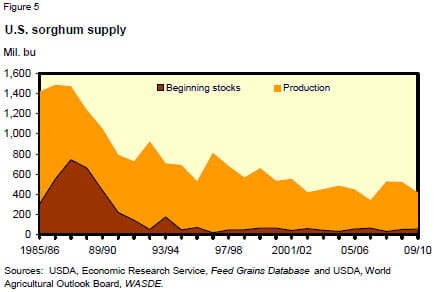

Sorghum Production Prospects Lowered

Sorghum production is forecast at 364 million bushels, down 26 million bushels from last month and down 108 million from last year. Planted area is 6.6 million acres, down 5 per cent from the previous forecast and down 20 per cent from 2008/09. All of the major sorghum producing States are at or below last year’s levels. This is the third lowest planted acreage on record. Area harvested for grain is forecast at 5.7 million acres, down 5 per cent from last month and down 22 per cent from last year.

Based on 1 October conditions, yield is forecast at 64.0 bushels per acre, down 1.5 bushels from September and down 1.0 bushel from 2008/09. The yield forecast in Kansas, the largest sorghum-producing State, increased 1.0 bushel from September. Producers in Texas, the second largest producing State, expect a yield of 44.0 bushels per acre, down 3.0 bushels from last month and down 8.0 bushels from last year.

Total sorghum supply for 2009/10 is projected at 418 million bushels, down 12 million from last month and down from 525 million a year earlier. Projected total utilization is 370 million bushels, down 10 million from last month, and down from 470 million from 2008/09. Feed and residual use is lowered to 140 million bushels, down 10 million from last month. Exports remain unchanged at 140 million as foreign demand for sorghum remains favorable. Ending stocks for 2009/10 were lowered 2 million bushels this month to 48 million.

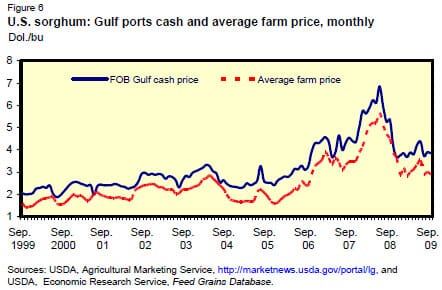

Prices for 2009/10 remain unchanged from last month at $2.60 to $3.20 per bushel. The season average price for 2008/09 was lowered 3 cents to $3.20 per bushel.

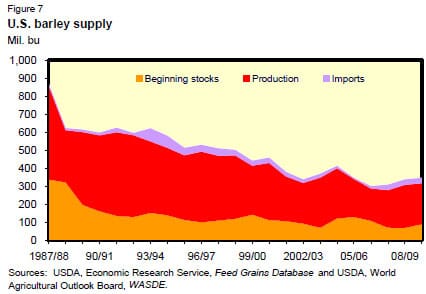

Barley Yield a Record

Barley production is estimated at 227 million bushels, up 20 million bushels from last month but 5 per cent below 2008. Average yield per acre, at 72.8 bushels, is up 7.0 bushels from last month and 9.2 bushels from last year and is the highest yield on record since estimates began in 1866. Producers planted 3.6 million acres for 2009, unchanged from last month but down 16 per cent from last year. This is the second lowest planted acreage on record. Area harvested for grain is estimated at 3.1 million acres and remains unchanged from last month, but is down 17 per cent from 2008.

Total supply of barley in 2009/10 is projected at 346 million bushels, up 21 million bushels due to the increase in production. Feed and residual use is estimated at 50 million bushels, down 10 million from last month and 17 million from 2008/09. Decreased feed and residual use lowers total use to 235 million bushels, down from 249 million last year. Ending stocks for 2009/10 are raised 31 million bushels this month to 111 million based on the 30 September Grain Stocks report.

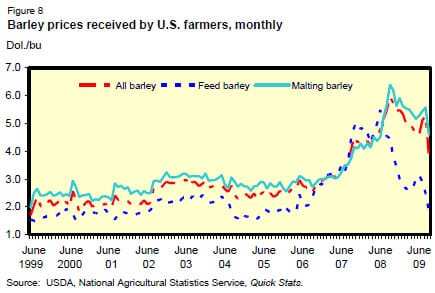

The 2009/10 projected barley farm price range is narrowed 10 cents on each end to $3.70-$4.20 per bushel, compared with $5.37 per bushel in 2008/09.

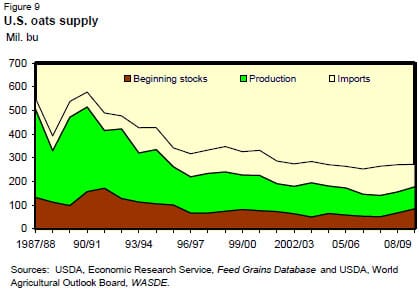

Oats Yield at Record High

Oats production in 2009/10 is estimated at 93 million bushels, up 1 million bushels from last month and up 4 million from 2008/09. The estimated yield is at a record high 67.6 bushels per acre, up 3.1 bushels from the last forecast and up 3.9 bushels from the previous year. Compared with last year, yields increased for most States in the western third of the country and for several Appalachian States. Harvested area is estimated at 1.4 million acres, down slightly from last month and last year. Area harvested for grain in 2009/10 is the smallest on record, continuing a steady downward trend.

Total supplies for 2009/10 are forecast at 272 million bushels, up 1 million from last month, as 2009/10 production is increased slightly. Ending stocks are projected at 74 million bushels, down 1 million from last month and down from 84 million in 2008/09.

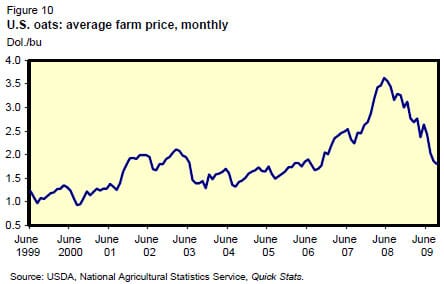

The 2009/10 projected oats farm price range is narrowed 5 cents on both ends of the range to $1.85-$2.15 per bushel, compared with $3.15 per bushel last year.

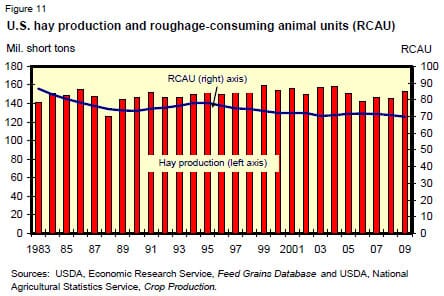

Hay Production up in 2009

All hay production in 2009 is forecast at 152.8 million tons, up 7 million from 2008 due to increased yields. The all-hay yield is expected to be 2.54 tons per acre, up from 2.43 tons per acre in 2008. Harvested acres are forecast at 60.2 million acres, up slightly from 60.1 million last year.

Production of alfalfa hay and alfalfa mixtures is forecast at 72.0 million tons, down 1.4 per cent from the August forecast, but up 3.4 per cent from last year. Based on 1 October conditions, yields are expected to average 3.43 tons per acre, down 0.05 tons from August but up 0.11 tons from last year. Harvested area is forecast at 21.0 million acres, unchanged from August, but up slightly from the previous year’s acreage. The largest yield increase is forecast in Pennsylvania, which is expecting a record-high yield of 3.7 tons per acre. Other States with record-high yields include Nebraska, Nevada, and Oregon.

Other hay production is forecast at 80.8 million tons, up 2 per cent from the August forecast and up 6 per cent from last year. Based on 1 October conditions, yields are expected to average 2.06 tons per acre, up 0.05 tons from August and up 0.11 tons from last year. This forecast matches 2004 as the record-high yield. Harvested area, at 39.2 million acres, is unchanged from the August forecast but up 113,000 acres from 2008.

Roughage-consuming animal units (RCAUs) in 2009/10 are estimated to be down slightly from 2008/09. With hay production up and RACUs down, hay supply per RCAU is 2.50 tons in 2009/10, compared with 2.36 tons in 2008/09.

World Coarse Grain Production Up Despite China Corn Reduction

Projected global 2009/10 coarse grain production increased 2.5 million tons this month to 1,092.5 million. Increased world barley production and increased US corn production more than offset a 5.0-million-ton drop in China’s corn.

This month, numerous revisions were made to coarse grain production in Sub- Saharan Africa, including the revision of sorghum and millet databases back to 2000. Previously, sorghum had been reported with millet for some countries, but starting this month, sorghum and millet production are reported separately for Cameroon, the Central African Republic, Chad, Congo (Kinshasa), Guinea, Guinea-Bissau, Mali, Sierra Leone, Togo, and Botswana. Additionally, the marketing year was shifted for Mozambique and Zimbabwe to move production into the first year of the split year, effectively treating these countries as importers, and differently from South Africa. The revisions that broke out sorghum from millet were the main reason foreign millet production declined 2.3 million tons and sorghum increased 2.1 million tons.

China’s corn production is forecast down 5.0 million tons at 155.0 million. Harvested area is revised up 0.5 million hectares to 30.0 million, slightly above the level of the previous year, as area responded to incentives, including Government intervention to support prices. However, hot dry weather during tasselling significantly reduced corn yields in Western Manchuria, a key corn-producing region. China’s average corn yield is projected down 5 per cent this month to 5.17 tons per hectare, down 7 per cent from an estimated record a year ago.

Reduced 2009/10 corn production is also projected this month for Russia, down 0.3 million tons to 4.7 million, as dryness limited yields; for Moldova, down 0.2 million tons to 0.8 million, as reduced area was reported; and for Colombia, down 0.2 million tons to 1.7 million, mostly due to reduced area. Drought in parts of Central America trimmed corn production prospects slightly in Guatemala and Nicaragua. Small reductions are also made this month for Ethiopia, Madagascar, Angola, Australia, Georgia, Tanzania, North Korea, and Lesotho.

Increased corn production is forecast this month for the United States; for the EU, up 0.7 million tons to 56.6 million due to improved yield prospects for Hungary and Romania; for Malawi, up 0.7 million tons to 3.7 million due to reported increases in both area and yield; for Ukraine, up 0.5 million tons to 9.0 million, because of strong reported yields; and for Canada, up 0.3 million tons to 9.7 million, based on yield surveys by Statistics Canada. There were smaller increases for Mozambique, Uganda, Somalia, Benin, and Swaziland.

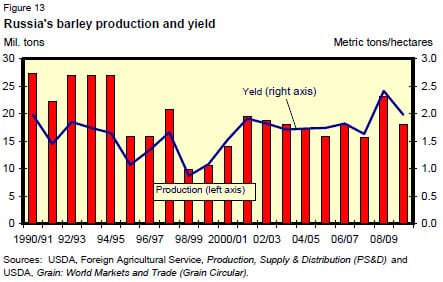

World barley production is projected up 4.4 million tons, more than offsetting the decline in corn of 1.5 million. The largest increase in barley production is for Russia, up 2.0 million tons to 18.0 million, based on yields reported from the Volga and Siberia. Volga yields were not hurt as much as expected by dryness, while growing and harvesting conditions in Siberia have been exceptionally good. Algeria’s barley production is revised up 0.7 million tons to 2.0 million, as exceptionally abundant rains encouraged a sharp area expansion and record yields. EU barley production is projected up 0.7 million tons to 61.5 million as increased production reported for France and Poland more than offset a reduction for Spain.

Barley production is boosted 0.3 million tons for Canada and 0.2 million for Australia. A late first frost helped barley harvest in Canada, while rains in southern and western Australia boosted production prospects. Smaller increases are estimated this month for Moldova and South Africa. Global oats and rye production increased slightly this month based on increased production of oats in Australia and oats and rye in the EU.

Increased 2009/10 Beginning Stocks Boost Supplies

Global coarse grain beginning stocks for 2009/10 are increased 2.2 million tons to 190.5 million, with most of this month’s increase in corn. Increased 2008/09 corn production was reported for Brazil, up 1.0 million tons to 51.0 million, and for South Africa, up 0.8 million tons to 12.8 million. The revised 2008/09 corn supply and demand boosts Brazil’s ending stocks 1.0 million tons to 12.4 million and increases South Africa’s stocks 0.9 million tons to 4.2 million. Statistics Canada’s reported grain stocks revealed a sharp reduction in grain feeding as animal numbers are declining. Canada’s coarse grain consumption estimated for 2008/09 was reduced, and ending stocks increased 0.8 million tons to 6.4 million. Partly offsetting these increases is a reduction in Argentina’s coarse grain stocks due to higher estimated exports in 2008/09.

Record 2009/10 Coarse Grain Use Boosted

World coarse grain use is projected to grow 3 per cent in 2009/10, twice as fast as estimates of growth in 2008/09. This is in keeping with reduced prices and stronger macro-economic growth. This month’s forecast of 2009/10 global use is up 4.1 million tons to 1,103.4 million, with corn use up 3.5 million tons to 803.1 million. With sharply higher production, world barley use is projected up 0.8 million tons this month to 147.1 million. Sorghum use is up 1.8 million tons to 64.2 million, mostly due to production revisions for Sub-Saharan Africa, but this increase is more than offset by the reduction in millet consumption.

The largest increase in projected 2009/10 coarse grain use is for China, up 1.4 million tons to 167.9 million. Corn feed use is up 1.0 million to support increasing meat production, and sorghum food and industrial use (mostly alcohol for human consumption) is also increased.

The EU, with increased production and reduced export prospects this month, is projected to feed 0.9 million tons more coarse grains, but with ample wheat supplies, food and industrial use is forecast slightly lower this month. Mexico’s projected coarse grain feed use is up 0.8 million tons this month in expectation of some growth from 2008/09 levels. Ukraine’s coarse grain feed use is also up 0.8 million tons due to increased corn production and to reflect expected meat production increases. Russia’s coarse grain use is up 0.6 million tons this month, with much larger barley production and limited export opportunities. Brazil’s feed use is up 0.5 million tons this month due to increased corn stocks and recovering meat exports. There are smaller increases this month for Algeria, Colombia, and several other countries. There are numerous changes in production and consumption for Sub-Saharan countries this month, but they are mostly offsetting, with total coarse grain use for the region up 0.4 million tons to 94.9 million.

The largest reduction this month in projected 2009/10 coarse grain use is for Canada, down 0.8 million tons as reduced animal numbers and declining feed use in 2008/09 dim future prospects. Argentina’s coarse grain use is projected down 0.6 million tons, with less feed use of sorghum and barley. Chile, Australia, and several other countries have smaller reductions in projected coarse grain use.

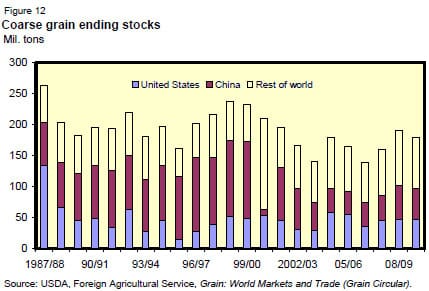

Global Coarse Grain Stocks Up Despite the Sharp Drop in China

World coarse grain ending stocks for 2009/10 are projected up 0.6 million tons this month to 179.7 million. Behind this small increase are some large increases and decreases for several countries.

China’s reduced corn production and increased use of corn and sorghum combine to cut forecast coarse grain stocks for the world’s largest holder by 6.5 million tons to 49.2 million tons. These are still large stocks, the equivalent of 3.5 months of projected 2009/10 use.

Other countries with reduced stocks prospects this month are Mexico, down 0.6 million tons due to increased feed use; Ukraine, down 0.3 million for the same reason; and Tunisia, Colombia, Nicaragua, Tanzania, Guatemala, and Libya, with smaller reductions.

More than offsetting the aforementioned declines in projected ending stocks are increases for the United States; the EU, up 1.5 million tons due to increased production and reduced export prospects; Russia, up 1.2 million tons due to increased barley production; South Africa, up 0.8 million tons because of large beginning stocks; Malawi, up 0.7 million tons on a bumper corn crop; Canada, up 0.6 million tons due to increased supplies and reduced use; Brazil, up 0.5 million tons based on increased beginning stocks; and Moldova, Algeria, Zambia, Argentina, Mozambique, Australia, and Kazakhstan, with smaller increases.

Global 2009/10 Coarse Grain Trade Reduced, US Corn Exports Cut

World coarse grain trade forecast for 2009/10 (October-September) is reduced 1.4 million tons this month to 111.0 million. Global corn trade is reduced 1.6 million tons to 84.8 million, but sorghum trade is increased slightly with higher expected exports for Australia.

Corn imports for Canada are cut 1.5 million tons to 2.0 million. Increased beginning stocks and production of coarse grains are boosting domestic supplies, while declining animal numbers are shrinking the demand for feed grains. Other corn import changes are smaller and mostly offsetting. Chile’s corn imports are trimmed 0.5 million tons as meat production prospects decline, but Colombia’s corn imports are increased 0.4 million due to stronger-than-expected poultry production. With reduced corn production, Russia and Georgia are expected to increase imports slightly, but large corn supplies are limiting corn import prospects for South Africa.

Foreign corn exports for 2009/10 are little changed this month, with Russia’s exports trimmed 0.15 million tons and Zambia increased 0.1 million due to production changes.

Further Reading

| - | You can view the full report by clicking here. |

October 2009