Total fisheries and aquaculture production is expected to reach 184.1 million tonnes in 2022 © David Hogsholt, FAO

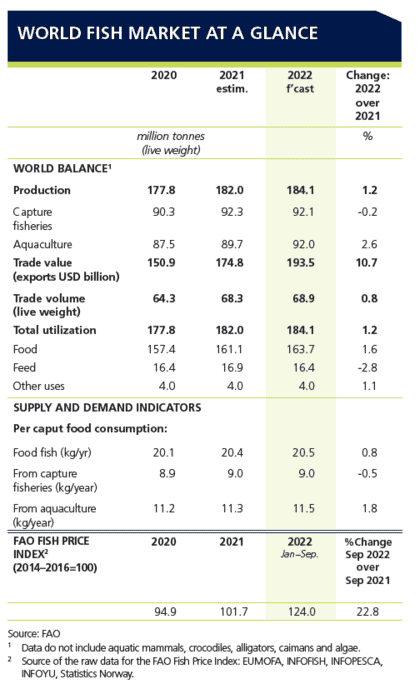

Total fisheries and aquaculture production is expected to increase globally by 1.2 percent in 2022 (+2.6 percent for aquaculture and -0.2 percent for capture fisheries) to reach 184.1 million tonnes, according to the latest analysis in the FAO’s Biannual food outlook.

The Biannual food outlook is the FAO’s report on global food markets. Its most recent iteration shows that market conditions are somewhat easing as we enter 2023. However, increased climate variability, conflicts and geopolitical tensions, bleak economic prospects, soaring agricultural input costs and export restrictions continue to pose challenges to global food commodity market stability.

Though global fisheries and aquaculture production is expected to increase globally by 1.2 percent in 2022, continued supply limitations and high inflation could cause prices to strengthen while a slowing global economy will likely increase price sensitivity.

Total fisheries and aquaculture production is expected to reach 184.1 million tonnes. Output from aquaculture is forecast to grow by 2.6 percent, remaining marginally behind its long-term growth rate (3.7 percent between 2015–2020), as producers grapple with high input costs and market uncertainties, such as high freight rates and reduced consumer purchasing power.

High fuel prices, lower quotas on major stocks and poor weather in some key fishing grounds have all contributed to a slowdown in capture fisheries, which is forecast to fall by 0.2 percent in 2022. Looking towards 2023, aquaculture production is forecast to continue to rise, while that of capture fisheries will remain essentially flat.

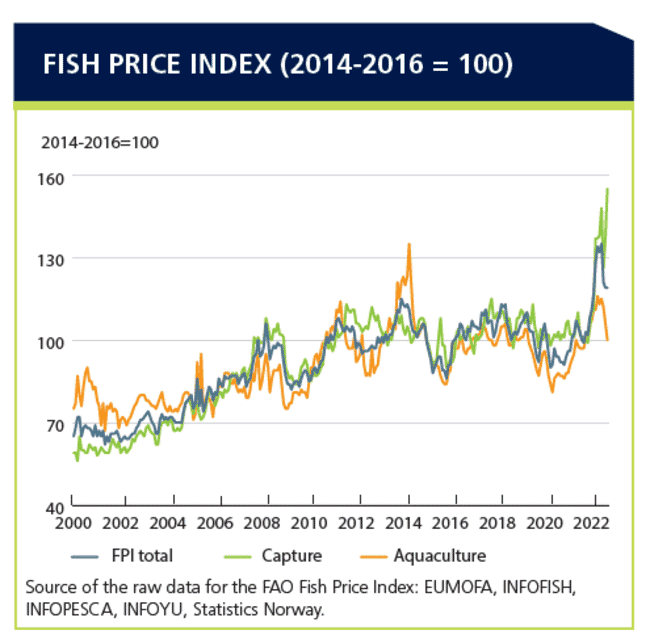

The FAO Fish Price Index (FPI) stood at 119 points in September 2022, down 16 points from June 2022, when overall fish prices reached historic highs due to revived demand following the pandemic slump. However, September 2022 prices remained strong compared with September 2021, demonstrating a 20-point rise in the FPI.

Prices of aquaculture products have since fallen back to previous levels, mainly because of reduced feed costs. A slowing global economy has reduced consumer purchasing power and is likely to increase price-sensitivity in the near future. Tighter supplies have kept prices of capture fisheries high, with limited quotas for key whitefish and small pelagic fisheries exerting upward pressure on prices.

Trade volumes in live weight equivalent are likewise forecast for 2022. However, the higher prices will lead to a substantial increase in the value of trade. Much of this growth will stem from record-breaking salmon prices in the first half of the year and sustained high prices for whitefish and small pelagics. Overall, the value of global trade is projected to increase from $174.8 billion in 2021 to $193.5 billion in 2022, which would represent a surge of 10.7 percent. Trade values had slumped in 2020, largely due to reduced volumes, before rising by 16 percent in 2021 as economies reopened. In particular, China (mainland), Chile, Ecuador and Norway will account for most of this increase.

Market indicators for 2023

Analysts with the FAO highlighted the global food import bill, developments in the ocean freight market and the global agricultural input import bill as key market indicators for the coming year.

When looking at the global food import bill – which came in at $1.94 trillion last year – analysts expect it to reach another record in 2022. The year-on-year increase will likely be less pronounced than in the previous year, owing to the falling purchasing power of importers at a time when food prices are at all-time highs. Worryingly, many economically vulnerable countries are paying more while receiving less food.

The global agricultural input import bill (IIB) is forecast to reach an all-time high of $424 billion in 2022, representing a near 50-percent increase from 2021 and reaching more than twice the level registered in 2020. This sharp increase is almost entirely on account of soaring costs of inputs, while growth in imported volumes remains subdued.

The report authors also highlight changes in ocean freight protocols, saying that these will hold sway on global food markets. Despite generally buoyant trade in grains and oilseeds, as well as challenging logistics in some areas, freight rates for the transportation of dry bulk commodities took a significant step down over the past six months, as geopolitical tensions, export restrictions and global recessionary fears weighed on market sentiment and curbed chartering activity.