The World Bank Group (WBG) Agriculture Action Plan 2013–151 summarizes critical challenges facing the global food and agriculture sector.

Global population is expected to reach 9 billion by 2050, and the world food-producing sector must secure food and nutrition for the growing population through increased production and reduced waste. Production increase must occur in a context where resources necessary for food production, such as land and water, are even scarcer in a more crowded world, and thus the sector needs to be far more effi cient in utilizing productive resources. Further, in the face of global climate change, the world is required to change the ways to conduct economic activities.

Fisheries and aquaculture must address many of these diffi cult challenges. Especially with rapidly expanding aquaculture production around the world, there is a large potential of further and rapid increases in fi sh supply—an important source of animal protein for human consumption. During the last three decades, capture fi sheries production increased from 69 million to 93 million tons; during the same time, world aquaculture production increased from 5 million to 63 million tons (FishStat). Globally, fi sh2 currently represents about 16.6 percent of animal protein supply and 6.5 percent of all protein for human consumption (FAO 2012). Fish is usually low in saturated fats, carbohydrates,

and cholesterol and provides not only high-value protein but also a wide range of essential micronutrients, including various vitamins, minerals, and polyunsaturated omega-3 fatty acids (FAO 2012). Thus, even in small quantities, provision of fish can be effective in addressing food and nutritional security among the poor and vulnerable populations around the globe.

In some parts of the world and for certain species, aquaculture has expanded at the expense of natural environment (for example, shrimp aquaculture and mangrove cover) or under technology with high input requirements from capture fisheries (for example, fishmeal). However, some aquaculture can produce fish efficiently with low or no direct input. For example, bivalve species such as oysters, mussels, clams, and scallops are grown without artificial feeding; they feed on materials that occur naturally in their culture environment in the sea and lagoons.

Silver carp and bighead carp are grown with planktons proliferated through fertilization and the wastes and leftover feed materials for fed species in multispecies aquaculture systems (FAO 2012).

While the proportion of non-fed species in global aquaculture has declined relative to higher trophic-level species of fish and crustaceans over the past decades, these fish still represent a third of all farmed food fish production, or 20 million tons (FAO 2012). Further, production effi ciency of fed species has improved. For example, the use of fishmeal and fish oil per unit of farmed fish produced has declined substantially as reflected in the steadily declining inclusion levels of average dietary fishmeal and fish oil within compound aquafeeds (Tacon and Metian 2008). Overall, a 62 percent increase in global aquaculture production was achieved when the global supply of fishmeal declined by 12 percent during the 2000–08 period (FAO 2012).

Many of the fishers and fish farmers in developing countries are smallholders. The Food and Agriculture Organization (FAO) estimates that 55 million people were engaged in capture fisheries and aquaculture in 2010, while small-scale fisheries employ over 90 percent of the world’s capture fishers (FAO 2012). To these small-scale producers fi sh are both sources of household income and nutrients, and sustainable production and improved effi ciency would contribute to improve their livelihoods and food security. Sustainably managing marine and coastal resources, including fish stock and habitat, would also help building and augmenting resilience of coastal communities in the face of climate change threats.

One important feature of this food-producing sector is that fi sh is highly traded in international markets. According to the FAO (2012), 38 percent of fish produced in the world was exported in 2010. This implies that there are inherent imbalances in regional supply and regional demand for fish, and international trade—through price signals in markets—provides a mechanism to resolve such imbalances (Anderson 2003). Therefore, it is important to understand the global links of supply and demand of fish to discuss production and consumption of fish in a given country or a region, while understanding the drivers of fish supply and demand in major countries and regions is essential in making inferences about global trade outcomes. Developing countries are well integrated in the global seafood trade, and fl ow of seafood exports from developing countries to developed countries has been increasing. In value, 67 percent of fishery exports by developing countries are now directed to developed countries (FAO 2012).

This report offers a global view of fish supply and demand. Based on trends in each country or group of countries for the production of capture fisheries and aquaculture and those for the consumption of fish, driven by income and population growth, IFPRI’s newly improved International Model for Policy Analysis of Agricultural Commodities and Trade (IMPACT model) simulates outcomes of interactions across countries and regions and makes projections of global fish supply and demand into 2030. Projections are generated under different assumptions about factors considered as drivers of the global fish markets. This report reflects a collaborative work between the international Food Policy Research Institute (IFPRI), the FAO, the University of Arkansas at Pine Bluff , and the World Bank. This work builds on the publication Fish to 2020 by Delgado and others (2003).

Throughout the report, the discussions are centered around three themes: (1) health of global capture fisheries, (2) the role of aquaculture in filling the global fish supply-demand gap and potentially reducing the pressure on capture fisheries, and (3) implications of changes in the

global fish markets on fish consumption, especially in China and Sub-Saharan Africa.

Findings and Implications

This study employs IFPRI’s IMPACT model to generate projections of global fish supply and demand. IMPACT covers the world in 115 model regions for a range of agricultural commodities, to which fish and fish products are added for this study. As is the case with most global modeling work, an important value that IMPACT brings to this study is an internally consistent framework for analyzing and organizing the underlying data. However, there are known data and methodology issues that arise from choices made by the key researchers for the purposes of maintaining computational tractability, internal analytical consistency, and overall simplicity. These are summarized in section 2.6.

Baseline Scenario

After demonstrating that the model successfully approximates the dynamics of the global fish supply and demand over the 2000–08 period, the outlook of the global fish markets into 2030 is projected under the scenario considered most plausible given currently observed trends (see table E.1 for key results). The model projects that the total fish supply will increase from 154 million tons in 2011 to 186 million tons in 2030. Aquaculture’s share in global supply will likely continue to expand to the point where capture fisheries and aquaculture will be contributing equal amounts by 2030. However, aquaculture is projected to supply over 60 percent of fish destined for direct human consumption by 2030. It is projected that aquaculture will expand substantially, but its growth will continue to slow down from a peak of 11 percent per year during the 1980s. The global production from capture fisheries will likely be stable around 93 million tons during the 2010–30 period.

Looking across regions, China will likely increasingly influence the global fish markets. According to the baseline model results, in 2030 China will account for 37 percent of total fish production (17 percent of capture production and 57 percent of aquaculture production), while accounting for 38 percent of global consumption of food fish.3 Given the continued growth in production projection, China is expected to remain a net exporter of food fish (net importer of fish if fishmeal is considered). Fast supply growth is also expected from aquaculture in South Asia (including India), Southeast Asia, and Latin America.

Per capita fish consumption is projected to decline in Japan, Latin America, Europe, Central Asia, and Sub-Saharan Africa. In particular, per capita fish consumption in Sub-Saharan Africa is projected to decline at an annual rate of 1 percent to 5.6 kilograms during the 2010–30 period.

However, due to rapid population growth, which is estimated at 2.3 percent annually during the 2010–30 period, total food fish consumption demand would grow substantially (by 30 percent between 2010 and 2030). On the other hand, projected production increase is only marginal. Capture production is projected to increase from an average of 5,422 thousand tons in 2007–09 to 5,472 thousand tons in 2030, while aquaculture is projected to increase from 231 thousand tons to 464 thousand tons during the same period. While the region has been a net importer of fish, under the baseline scenario, its fish imports in 2030 are projected to be 11 times higher than the level in 2000.

As a result, the region’s dependency on fish imports is expected to rise from 14 percent in 2000 to 34 percent in 2030. Looking across species, the fastest supply growth is expected for tilapia, carp, and Pangasius/catfish. Global tilapia production is expected to almost double from 4.3 million tons to 7.3 million tons between 2010 and 2030.

The demand for fishmeal and fish oil will likely become stronger, given the fast expansion of the global aquaculture and sluggishness of the global capture fisheries that supply their ingredients.

During the 2010–30 period, prices in real terms are expected to rise by 90 percent for fishmeal and 70 percent for fish oil. Nonetheless, with significant improvements anticipated in the efficiency of feed and management practices, the projected expansion of aquaculture will be achieved with a mere 8 percent increase in the global fishmeal supply during the 2010–30 period. In the face of higher fishmeal and fish oil prices, species substitution in production is also expected, where production of fish species that require relatively less fish-based feed is preferred.

Scenario Analysis

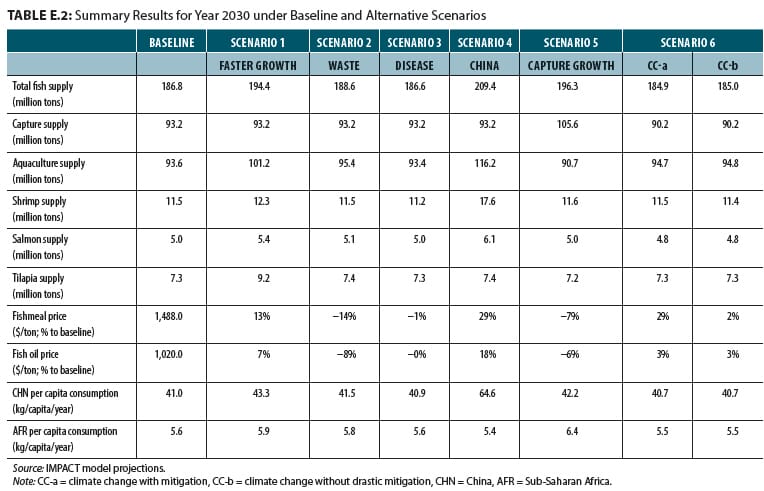

Besides the baseline (most plausible) scenario, six additional scenarios are implemented to investigate potential impacts of changes in the drivers of global fish markets (table E.2).

Scenario 1 addresses the case where all aquaculture is able to grow faster than under the baseline scenario by 50 percent between 2011 and 2030. In particular, the scenario assumes faster technological progress such that aquaculture would be able to supply a given amount at a lower cost (supply curves would shift outward), but it assumes the same feed requirements per unit weight of aquaculture production. Technical progress may include genetic improvement, innovations in distribution, improvements in disease and other management practices, control of biological process (life cycle) for additional species, and improvements in the condition of existing production sites and expansion of new production sites. While these technical changes are implicit in the baseline parameters, this scenario accelerates the changes by 50 percent. At the global level, the model predicts that aquaculture production in 2030 would expand from 93.2 million tons under the baseline case to 101.2 million tons under this scenario. The model predicts that the faster

growth in all aquaculture would stress the fishmeal market and this effect would dictate which species and which regions would grow faster than the others. Under this scenario, tilapia production in 2030 would be 30 percent higher than in the baseline case; production of mollusks, salmon, and shrimp in 2030 would be higher by more than 10 percent. As a result, relative to the baseline scenario, all fi sh prices in 2030 in real terms would be lower by up to 2 percent, except for the price of the other pelagic category, which is used as an ingredient of fi shmeal and fi sh oil. Fishmeal price in 2030 would be 13 percent higher than in the baseline case, while fish oil price would be higher by 7 percent.

Scenario 2 investigates how expanded use of fish processing waste in fishmeal and fish oil production might affect the market of these fish-based products, where, in addition to the baseline countries, all countries that produce fishmeal or fish oil are now assumed to have the option to use waste in their production starting in 2011. Aquaculture expansion has relied in large part on improvements surrounding feed, including feed composition for nutrition and digestibility as well as cost effectiveness, genetics of fish, and feeding techniques and practices. While anticipated continuation of these improvements is already incorporated in the baseline parameters, this scenario addresses possible expansion of feed supply by utilizing more fish processing waste in the production of fishmeal and fish oil. The model indicates that fishmeal production in 2030 would increase by 12 percent and fishmeal price would be reduced by 14 percent relative to the 2030 results in the baseline case. This would boost the aquaculture production of freshwater and diadromous fish, salmon, and crustaceans. Although cost is involved in selection, collection, and reduction of fish waste, use of the additional feedstock represents a great opportunity to increase fishmeal and fish oil production, especially where organized fi sh processing is practiced.

For example, 90 percent of the ingredients used in fishmeal produced in Japan come from fish waste (FAO data).5 Globally, about 25 percent of fishmeal is produced with fish processing waste as ingredient (Shepherd 2012). Increased use of fish waste would reduce the competition for small fish between fishmeal production (that is, indirect human consumption) and direct human consumption.

Scenario 3 introduces a hypothetical major disease outbreak that would hit shrimp aquaculture in China and South and Southeast Asia and reduce their production by 35 percent in 2015. The model is used to simulate its impact on the global markets and on production in affected and unaffected countries between 2015 and 2030. Results suggest that countries unaffected by the disease would increase their shrimp production initially by 10 percent or more in response to the higher shrimp price caused by the decline in the world shrimp supply.

However, since Asia accounts for 90 percent of global shrimp aquaculture, the unaffected regions would not entirely fill the supply gap. The global shrimp supply would contract by 15 percent in the year of the outbreak. However, with the simulated recovery, the projected impact of disease outbreak on the global aquaculture is negative but negligible by 2030.

Scenario 4 is a case where consumers in China expand their demand for certain fish products more aggressively than in the baseline case. The scenario is specified such that Chinese per capita consumption of high-value shrimp, crustaceans, and salmon in 2030 would be three times higher than in the baseline results for 2030 and that of mollusks double the baseline value. These are higher-value commodities relative to other fi sh species and, except for mollusks, they require fishmeal in their production. Under this scenario, global aquaculture production could increase to more than 115 million tons by 2030. This scenario would benefit the producers and exporters of these high-value products, such as Southeast Asia and Latin America. While overall fish consumption in China in 2030 would be 60 percent higher relative to the baseline case, all other regions would consume less fish by 2030. For Sub-Saharan Africa, per capita fish consumption in 2030 would be reduced by 5 percent under this scenario, to 5.4 kilograms per year. Fishmeal price in 2030 in real terms would increase by 29 percent and fish oil price by 18 percent relative to the baseline case. Over 300 thousand tons more of fishmeal would be produced, by reducing additional 1 million tons of fish otherwise destined for direct human consumption.

Senario 5 simulates the impacts of productivity increase of capture fisheries in the long run where fisheries around the globe let the fish stocks recover to the levels that permit the maximum sustainable yield (MSY). In The Sunken Billions (Arnason, Kelleher, and Willmann 2009), it is estimated that eff ectively managed global capture fi sheries are assumed to sustain harvest at 10 percent above the current level. In this scenario, a gradual increase in the global harvest is assumed, achieving this augmented level in 2030. If this scenario were to be realized, the world would have 13 percent more wild-caught fish by 2030, relative to the baseline projection. In this scenario the resulting increase in the production of small pelagic and other fish for reduction into fishmeal and fish oil would reduce the pressure on the feed market, which results from the rapid expansion of aquaculture production that is expected to continue. Fishmeal price is expected to be lower by 7 percent than under the baseline case. Production in all regions would benefi t from this scenario. In particular, Sub-Saharan Africa would achieve fish consumption in 2030 that is 13 percent higher than under the baseline scenario. This is because increased harvest is likely to be consumed within the region, rather than being exported. Distributional implications of the scenario would be even higher if stock recovery process is accompanied by eff orts to substantially reduce inefficiency often prevalent in the harvest sector. Though confounded with losses due to lower-than-MSY yield, the cost of inefficient harvest sector is estimated to amount to $50 billion each year at the global level (Arnason, Kelleher, and Willmann 2009). On the other hand, relative abundance of fish would dampen fish prices so that aquaculture production in 2030 would be reduced by 3 million tons relative to the baseline case.

Scenario 6 considers the impacts of global climate change on the productivity of marine capture fisheries. Changes in the global fish markets are simulated based on the maximum catch potentials (maximum sustainable yield, MSY) predicted by Cheung and others (2010) under two scenarios: one with mitigation measures in place so that no further climate change would occur beyond the year 2000 level and the other with continuing trend of rising ocean temperature and ocean acidification.

Their mitigation scenario yields a 3 percent reduction in the global marine capture fisheries production in 2030 relative to the baseline scenario, while no-mitigation scenario would result in marginal additional harm to the capture fisheries at the global level (reduction of harvest by 0.02 percent in 2030). While the aggregate impact is negligible, distribution of the expected changes in catches widely varies across regions. In principle, high-latitude regions are expected to gain while tropical regions lose capture harvest (Cheung and others 2010). The highest gains are expected in the Europe and Central Asia (ECA) region (7 percent) and the largest losses in the Southeast Asia (SEA; 4 percent) and East Asia and Pacific (EAP; 3 percent) regions. The model predicts that market interactions will attenuate the impact of the changes in the capture harvest and its distribution. Aquaculture will likely increase its production to off set the small loss in the capture harvest. Imports and exports will likely smooth the additional supply demand gap caused by the changes in capture harvest, and fish consumption levels in 2030 are not expected to change in any region due to climate change. The simulated loss in global catches is relatively small in part because this study provides medium-term projections into 2030, whereas climate change is a long-term phenomenon. Given the structure of the IMPACT model, many small island states were grouped together in the “rest of the world” (ROW) model region. Therefore, this simulation exercise is unable to analyze the impact of climate changes in small island states, including Pacific island countries and territories.

Overall Lessons

We have developed a rigorous analytical tool that is capable of making projections on the implications of the ongoing shifts on global fish production and reallocation of fish supply through international trade. The model, though with known limitations, is successfully calibrated

and employed to evaluate different policies and alternative events and to illustrate likely evolution of the global seafood economy.

From the modeling exercise and scenario analyses, it is clear that aquaculture will continue to fill the growing supply-demand gap in the face of rapidly expanding global fish demand and relatively stable capture fisheries. While total fi sh supply will likely be equally split between capture and aquaculture by 2030, the model predicts that 62 percent of food fi sh will be produced by aquaculture by 2030. Beyond 2030, aquaculture will likely dominate future global fish supply.

Consequently, ensuring successful and sustainable development of global aquaculture is an imperative agenda for the global economy. Investments in aquaculture must be thoughtfully undertaken with consideration of the entire value chain of the seafood industry. Policies should provide an enabling business environment that fosters efficiency and further technological innovations in aquaculture feeds, genetics and breeding, disease management, product processing, and marketing and distribution. The same is true for capture fisheries—developing enabling environment through governance reforms and other tools represents the first step toward recovery of overharvested fish stock and sustainability of global capture fisheries.

February 2014