“I was asked to give a presentation on this at last week’s North Atlantic Seafood Forum. The coronavirus is still very much a wildcard – we don’t know how much it will spread so it’s hard to read the markets right now – but we came up with four different scenarios, none of them good,” reflects Dr de Jong.

“And since I first prepared the presentation, we’ve already gone from the least bad option to somewhere between the third and second worst,” she adds.

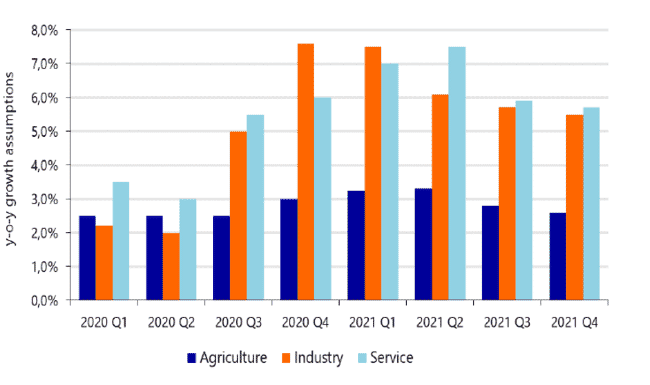

As a result, looking at the macro-economic situation, Dr de Jong predicts that the impact of the virus looks likely to be closer to that of the 2008 global financial crisis of 2008-2009, rather than to SARS – due to the fact that the Chinese and global economies are much more closely linked since the outbrak of the latter, back in 2003.

“The Chinese economy and the global economy are so closely linked, with many countries heavily dependent on China for manufacturing their goods, as a market for their exports and as a source of tourists,” she explains. “If the forecast for the Chinese economy to grow 2 percent slower than anticipated in 2020 is correct, then global growth rates will drop by 1 percent.”

Looking at the food and agriculture sectors, Dr de Jong notes that the restaurant and food service businesses are being hit the hardest – a trend compounded by the timing of the outbreak in the run-up to Chinese New Year. And, although many provinces of China are beginning to lift movement restrictions, there’s no sign of an immediate recovery.

“The initial forecast was for the Chinese economy to start to rebound in Q2, but we now think that it’s not going to happen until Q3 or Q4. And, looking ahead, while industrial production is beginning to rebound, consumer spending is lagging behind,” explains the Rabobank analyst.

And the slow rebound in consumer spending is not just hitting the Chinese food service sector.

“The Chinese food service sector is being hit as consumers in China are eating at home, while the sector in countries such as Singapore, Thailand and Vietnam is being impacted too, due to the decrease in tourism numbers,” she says.

Looking specifically at the seafood sector, Dr de Jong says that local production has not been too severely impacted other than in Hubei – the province at the heart of the outbreak – where freshwater production of species such as crayfish has been reduced by the raft of governmental restrictions.

In terms of seafood imports to China it is, once again, those typically destined for the food service sector that are being hit the hardest.

“Demand for products such as oysters, lobsters as well as the tuna and salmon that are favoured for sushi and sashimi has declined the most, while demand for the sort of products that are more commonly cooked and eaten at home – like pangasius and tilapia – has not been so impacted,” says Dr de Jong.

And, given that China is already experiencing something of a protein shortage, due to the impact of African swine fever on pork supplies, there’s scope for some growth in sales in products such as these. However, overall, Dr de Jong believes that “even in the best case scenario, the trend in Chinese seafood consumption in general will be flat”.

Looking beyond China, Dr de Jong says it’s too early to quantify the overall effect of the pandemic.

“It’s too early to say what the impact of the spread of the virus will be on other countries – such as Italy, for example,” she says.

However, despite the global concerns about the virus, there is some cause for optimism – with China’s containment strategy appearing to bear fruit. As Fish Site contributor, Ronnie Jin, told the site today: “no provinces have reported any new cases for the last three days except Wuhan. For the rest of us the lockdown is over and everything is back on track.”