The European market for shrimp is weak

The retail chain segment has reduced its orders significantly and stocks are said to be piling up as a result of consumers’ lessening purchase power and reluctance to buy comparatively expensive products.

Demand is decreasing on all major shrimp import markets. Import annual figures for 2008 indicate that shrimp imports decreased by 7 per cent in Spain, by 2 per cent in France and by 8 per cent in the United Kingdom and by 1 per cent in Germany compared with 2007.

In general, demand decreased more particularly for expensive shrimp products, such as processed products, chilled products or value-added products but that was not always the case, depending on the market and on the period, with fairly good end-of-year consumption.

US economic crisis impact shrimp market

The US economy has spiralled into what many analysts see as the worst recession and financial crisis since the Great Depression that begun with the crash of 1929. Whilst the food sector is one of the few that has not shown such a strong deterioration, the economic downturn has negatively affected some of the most significant areas of seafood consumption, such as tourism and the restaurant business, with considerable drops in sales. One of the strategies adopted by households is the reduction of casual dining in restaurants, preferring to eat more at home.

A report of shrimp sales from The Perishables Group shows that retailers are reducing their promotions for high-value seafood products like shrimp, and consequently, sales showed a reduction in terms of volume and value, at the end of 2008. However, this lack of demand has eased the pressure on prices, as supply remains sufficient; therefore, prices might give some space to encourage consumption in the short term.

A Closer Look at Europe

Argentina, Ecuador and China share the lead on the Spanish market

Compared with 2007 figures, 2008 annual Spanish shrimp imports lost 7 per cent in volume and 3 per cent in value. The decline in imports is not consistent across all products but differs according type. In 2008, 94 per cent of total Spanish shrimp imports were warmwater frozen whole products. In this category, the decrease was 6 per cent, while chilled products decreased by 26 per cent, coldwater frozen products by 19 per cent, whereas processed products registered a remarkable 23 per cent increase.

During the last quarter of 2008, when the economic crisis started to have a serious impact on European markets, Spanish shrimp imports remained fairly good with 56 000 tonnes, corresponding to only a 1 per cent decrease in volume on 2007 figures and to an 11 per cent increase in value.

Argentina, Ecuador and China shared the majority of shrimp exports to the Spanish market with 17 per cent market shares respectively.

Strong imports by France notwithstanding the economic crisis

French shrimp imports in 2008 for all categories combined were 2 per cent lower compared to 2007 figures but were nonetheless very good compared with previous years. In terms of value, imports were stable.

The 2008 decrease in volumes – compared with outstanding results in 2007 - affected all categories. However, while frozen whole imports decreased by only 1 per cent, higher-priced products such as fresh (-6 per cent) and processed ( 8 per cent) products experienced a more drastic drop, which is not surprising in a period of economic slow down.

Shrimp becomes less affordable to UK consumers

Repercussions of the economic crisis are particularly strong in the UK food sector. The economic recession is driving consumers away from expensive products, including shrimp, and from restaurants where shrimp is mainly consumed. In this context, it is not surprising that demand for shrimp, considered a “luxury” food item, has decreased substantially recently.

The average unit value for shrimp on the UK market in 2008 was as high as GBP 4.18/kg against GBP 3.72/kg in 2007, while frozen whole coldwater products recorded an even greater increase of 0.85 cents/kg.

UK annual import figures indicate that in 2008 UK total shrimp imports decreased by 8 per cent in volume and by 3 per cent in value. All categories were affected by the drop and in particular, the frozen sector decreased by 9 per cent, the chilled sector by 17 per cent and the prepared and preserved sector by 8 per cent.

The German shrimp market is rather static

The fact that Germany entered into recession during the third quarter of 2008, and registered a further 2.1 per cent decrease of its GDP in the fourth quarter of 2008, did not have a drastic impact on its shrimp sector. German shrimp imports, which had developed steadily at a strong growth rate during the past few years, settled down in 2008, decreasing only slightly (by 1 per cent in volume and by 4 per cent in value).

As in other European countries, the decrease in shrimp imports is mainly due to a reduction in fresh (-70 per cent of imports, on 2007 figures) and processed (-5 per cent) product demand. Lowered purchasing power and increased uncertainty push consumers towards to less expensive products. Total whole frozen shrimp imports were more or less stable and entered the German market at an average unit value of EUR 5.21/kg against EUR 6.60/kg for C&P products and EUR 9.93/kg for fresh products.

Details in the US Shrimp Industry

New antidumping duties and no more bonding requirements

The US Department of Commerce (DOC) published the new preliminary decisions on antidumping duties for Ecuador, India, Thailand, Viet Nam and China, resulting from the third administrative review. For these countries, the review considered sales to the US market between 1 February 2007 and 31 January 2008, except Ecuador, for which the period considered was 1 February 2007 to 14 August 2007.

This is because the US Trade Representative revoked the antidumping duty order on Ecuador effective 15 August 2007. The results of the review recommended a reduction in antidumping duties on Indian products from 110 companies, from a previous 1.69 per cent, to a 0.79 per cent average, decreasing to 0.39 per cent for one of the reviewed companies.

As for Viet Nam, the review set duties that range between 1.66 per cent for one economic group of producers, to 9.84 per cent for another group, while the rate that will be applied to the companies that were not studied was set at 25.76 per cent. In the case of Thailand, the two analyzed companies had their margins set at 4.25 per cent and 4.64 per cent, while the remaining 134 exporters will be given a 4.51 per cent duty.

Despite the economic turmoil, shrimp imports showed a slight increase during 2008

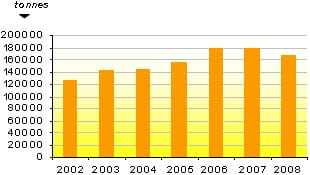

US shrimp imports totalled 564 000 tonnes worth USD 4 093 million, which represents a 1.3 per cent and 4.8 per cent increase in terms of volume and value respectively, compared with the 557 000 tonnes worth USD 3 904 million in 2007. Consequently, the unit value of imports grew 4 per cent. This positive trend was shown in almost all the main import categories, except other frozen preparations and 15 or less count of headless shell-on frozen, which showed lower trade both in volume and value.

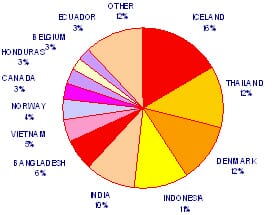

Headless shell-on shrimp accounted for 43 per cent of total imports of shrimp, both in volume and value, followed by peeled frozen shrimp, with a 33 per cent share in both indices. 70 per cent of the total supply of headless shell-on frozen shrimp originated in four countries, Thailand (24 per cent), Ecuador (18 per cent), Indonesia (15 per cent), and Mexico (13.5 per cent).

Thailand remains the main supplier of shrimp to the US accounting for 34 per cent of total imported volume (32 per cent in terms of value). However, purchases from this country fell in volume (-3 per cent), although in terms of value they grew 4 per cent, with a 7 per cent increase in unit value. Viet Nam and Indonesia showed a very good performance on sales of shrimp to the US (+42 per cent and +22 per cent respectively in terms of volume), while China showed a minor reduction (-1 per cent).

The European Outlook

In nearby all European countries, consumers have changed their habits to adapt to new economic constraints. The trend which includes saving on restaurant visits and on expensive food items is expected to last for some time. All EU countries are predicting more difficult times and worsening economic situation for all of 2009, giving little likelihood that comparatively expensive food items, such as shrimp, will register an increase in demand.

The period of Lent (40 days before Easter) is normally a good period for seafood consumption, particularly in Southern Europe where the Christian rituals are more closely observed. However, this year, demand seems to be below expectations. It appears, though, that European consumers are not ready to give up with festive food and that they are ready to pay higher prices occasionally on high quality products, such as wild-caught products or organic products.

US to Adapt to Changing Market

The global crisis has limited the availability of credit to everyone, and access to credit facilities has become more expensive. In a climate of uncertainty about the future behaviour of the market, these trends increase the costs of building stocks. Therefore, purchases are mainly to recompose the supply. On the other hand, the Thai Shrimp Association announced at the end of 2008 that it would reduce production by 20 per cent in order to adjust supply to lower demand. This should result in a lower supply of shrimp, which in turn should help maintain higher prices.

Consumers are becoming more price sensitive, which implies that the value-chain will have to look for ways to reduce their costs in order to avoid a price increase. Farmed shrimp has led to a reduction in the overall prices of shrimp. This opens a way for distributors to market shrimp as an affordable yet luxurious product. Prices of shrimp during 2008 did not have significant ups and downs. On the contrary, they remained fairly stable, peaking in August for white aquacultured shrimp, and by the end of the year, except for some particular products, prices were near or below the level registered at the beginning of 2008.

May 2009