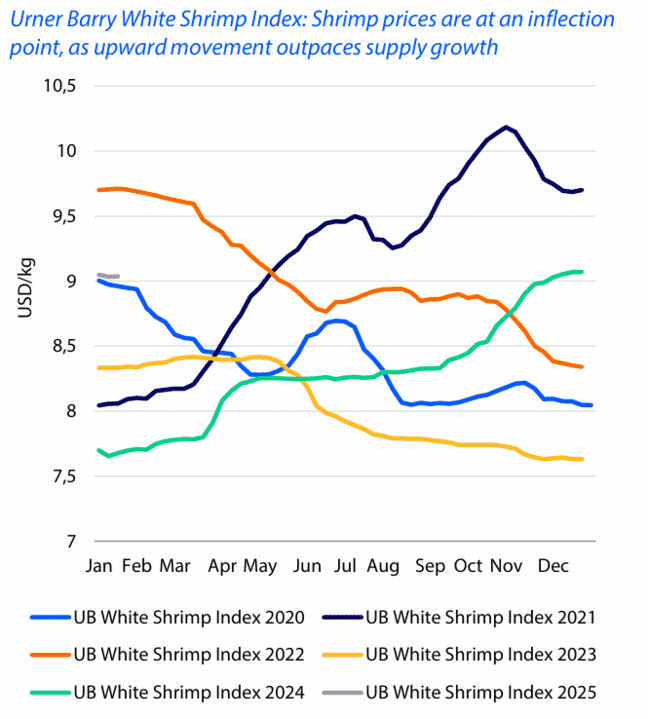

Prices in 2025 have started on a par with those in January 2020 © Urner Barry

The report, which was published this week, notes that: “The global shrimp industry is currently undergoing a period of rebalancing as producers slow production growth to reduce the demand-supply gap. This will lead to a gradual recovery in prices. The anticipated slowdown in supply growth is expected to alleviate the oversupply situation.”

The report predicts that Asian shrimp production is finally expected to recover, driven by gradual improvements in demand in the US and EU. However, it adds a caveat that the combination of weak demand in China, coupled with Ecuador's investment in value-added processing – which will allow the South American nation to diversify its product offerings, in line with Western market demand – could limit this growth.

The salmon story

Meanwhile Rabobank forecasts that salmon prices are expected to remain high, despite a global supply growth of 1 to 2 percent in H1 compared to the low volumes in the same period last year.

In Norway, more suitable sea temperatures and better coverage of winter sore vaccinations offer optimism for better productivity. Yet early harvests of small fish in late 2024 due to sea lice and jellyfish pressures have contributed to a lower standing biomass, thus the limited growth potential.

Equally, in Chile, they note that low biomass growth suggests tight salmon supplies. However, expected cooler water temperatures following El Nino are likely to enhance biological conditions, resulting in lower mortality rates and improved harvest weights, which should contribute to supply growth of around 2 to 3 percent.

After a period of high prices, salmon is becoming more price competitive relative to other proteins and Rabobank expects salmon prices to remain strong, albeit slightly below early 2024 peaks, due in part to a recovery in superior-grade fish supply from Norway.

Furthermore, the reduced rates of inflation are expected to improve demand in the West, unless Trump’s return to the US presidency prompts trade war-induced inflation.

“Despite challenges, salmon remains relatively affordable compared to other high-priced animal proteins, potentially attracting cost-conscious consumers and boosting demand. This, combined with lower anticipated biological and feed costs, should mark an inflection point in profitability in the first half of 2025,” the report states.

© Kontali and Rabobank

Feed ingredients

1. Marine

In terms of marine ingredients, the report notes that the advent of La Niña in the second half of 2024 and is expected to positively influence fishmeal supply. Peru's anchovy quota of 2.51 million tonnes for the second fishing season of 2024 marked a 49 percent increase from the same period in 2023 and 2025 is expected to be one of Peruvian fish meal and fish oil supply’s stronger years.

According to IFFO, if the full quota is harvested, it could add 500,000 tonnes of fish meal and 60,000 to 80,000 tonnes of fish oil to the global supply.

Despite a favourable quota announcement, fish meal remains relatively expensive compared to soymeal. Fishmeal prices are likely to face mild downward pressure, as Chinese inventory levels remain high, and demand is expected to soften as Chinese buyers complete a round of interim stockpiling.

“A combination of cheaper alternatives and high Chinese inventories suggest a mild price correction for fishmeal in 1H 2025, assuming no unforeseen supply issues in the soy and fish meal industries,” the report explains.

2. Terrestrial

Meanwhile China's grain and oilseed stockpiles, especially soybeans, are reaching record levels in anticipation of a trade war.

"Recent favourable seasons in the US, Brazil and Argentina are expected to create a soymeal surplus, further depressing prices in 2025," Rabobank concludes.