Farmed salmon. The supply of farmed salmon is projected

to grow around 12 percent in 2012, with exporters looking

to new markets such as Brazil, Russia, China and India.

Shipments to these markets increased by 20 percent in 2011,

reaching more than 210 000 tonnes.

Long-term growth in the EU and US markets is also

positive, as are recent developments in the Japanese market.

Consumption of 2011 farmed salmon increased 7 percent in

the EU, 10 percent in the US and 30 percent in Japan. The

long-term prospects for fish consumption in Japan remain

negative because of an ageing and stagnating population.

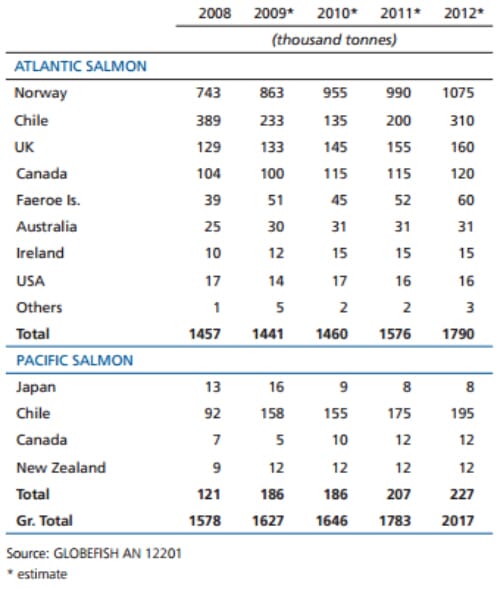

In Norway, production has risen 33 percent since 2008,

with new growth projected for 2012. Chile saw the strong

production growth of 2011 continue during early 2012.

Its 2011 salmon exports totalled almost 260 000 tonnes,

up more than 50 percent. In value terms, the increase was

even higher 63 percent, totalling USD 1.9 billion. South

American countries now account for 32 percent of Chiles exports, reaching 47 000 tonnes in 2011, with Brazil as the

main market in the region.

Prices of Salmon in Europe, Origin Norway

Wild salmon. Wild Pacific salmon remains important in overall supply, representing about 30 percent of the total market. In recent years, wild salmon harvests have been around 1 million tonnes annually, but there can be large annual swings. A large portion of wild salmon is shipped to China for processing and re-export.

|

| Global Farmed Salmon Production |

SMALL PELAGICS MACKEREL, HERRING, SARDINES

Mackerel. New fish migration patterns are causing

headaches for mackerel fishing nations in Northern Europe.

Despite negotiations among the EU, Norway, Iceland and the

Faroe Islands during early 2012, there is still no agreement

on a total mackerel quota. As a result, the unilateral quotas

are too high, with parties in the conflict accusing each other

of acting irresponsibly.

Meanwhile, Norwegian mackerel exports declined 11

percent in volume last year, but prices were up significantly.

Japan was the main market, importing 75 200 tonnes in 2011,

a 5 percent increase, followed by China with 57 700 tonnes,

up 13 percent, and Turkey, which had a 26 percent decrease.

Thanks to improved catches, Norways mackerel export volumes

recovered during the first quarter of 2012 by 21 percent, to

58 000 tonnes. China is now importing more mackerel from

Norway, but most of this is re-exported to Japan.

With higher mackerel catches anticipated in the short run,

the high prices experienced lately may come down during

the next quarter.

Herring. Herring has had a bonanza, due to lower catches

that pushed prices sky high during 2011 and early 2012,

with prices now 60 percent higher than a year ago.

Norwegian catches and export volumes continued to decline

during early 2012.

Canned sardines. The canned sardine market in Europe

continues to decline. Shipments of sardines to the three most

important European markets France, UK and Germany

fell a further 18 percent last year, with the largest reduction

registered in France where imports fell from 16 700 tonnes

in 2010 to 12 300 tonnes in 2011. The main supplier to all

three markets was Morocco, followed by Portugal.

June 2012