A Difficult Year Ahead?

Since mid April cracks have appeared in the global economy,

with a lacklustre tone evident in the local economy. Quarterly

movements in surveyed unemployment has been volatile of

late, with unemployment beneficary numbers dipping and job

advertising indicating a more modest recovery in the demand

for labour.

A large fall in the latest retail trade volumes revealed

an unwinding in the rugby World Cup-induced boost in cash

spending. This is a clear negative for quarter one GdP, which is

expected to be partly offset by climbing manufacturing sector

activity. A good start to the year for manufacturing sector activity

was evident in good primary production and encouraging export

statistics. however, the large fall in the April PmI (performance

of manufacturing index) figures suggests that the still high kiwi

dollar, a wobbly global scene and delays with the Canterbury

rebuild are likely to contribute to a difficult year ahead.

Two of the key potential transmissions mechanisms to the

New Zealand economy; namely funding and commodity

prices, have provided more positive signs. The NZ dollar has

started to play catch-up, reconnecting somewhat with falling

commodity prices. Technically, the New Zealand dollar doesnt

look extended at all based on where commodity prices currently

are (still high by historical standards). however, this does not

allow for the fact that a sizeable chunk of the export sector is

not benefiting from high commodity export prices (particularly

services and manufacturing).

Commodity prices fell sharply in April, to sit at an 18-month

low. Sheepmeat and wool prices dropped to 18-month lows.

International dairy prices have retracted back to the level that

prevailed in August 2010. historically, the aggregate level of

commodity prices are 12 percent higher than the 2000-09

decade average, propped up by meat and dairy prices. however,

the sub-groups of seafood, forestry, aluminium and horticulture

prices are below period averages.

What Will Grow the Economy?

An important pre-condition to the economy strengthening

this year will be for consumer sentiment to start marching to

the more upbeat tune already evident in business confidence

gauges. With the housing market data appearing to have paused

for breath and with mother Nature having already leant support

to the rural sector, the economy is looking devoid of a real

economic engine in the second half of the year. much depends

on business investment and the Christchurch rebuild as growth

engines over the next 12 months.

Specifically, it is uncertain times for commercial fishing in New

Zealand but the outlook is promising. more recently, the New

Zealand dollar has moved towards a more competitive level; and

an increasing share of the national catch is being exported to

developing markets, which have been relatively insulated from

the European sovereign debt crisis.

Export Statistics

Export NZ$Free On Board

All figures in this section are based on export data provided by Statistics New Zealand and analysed by the New Zealand Seafood Industry Council. Please note that the results for January, february and march (Q1) 2012 are provisional.

Export Tonnes

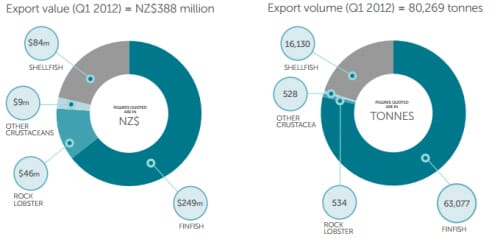

Exports of finfish species accounted for 64 percent of all seafood exports in dollar terms yet represent 79 percent of tonnes sold. While we export slightly more than 2,000 tonnes of rock lobster a year (about one percent of all catch), this species contributes around 14 percent to export earnings, although the contribution is down slightly in the first quarter as most rock lobster is caught towards the end of the year.

Export earnings in Q1 were up 8.6 percent compared with Q1 2011. Volumes were also up albeit to a lesser extent at 3.2 percent.

The volume and value of other crustaceans (mainly crab, shrimps and prawns) grew strongly between years, up 59 percent and 41

percent respectively.

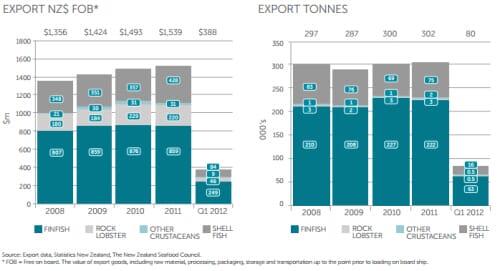

The total quantities exported fell somewhat as the world came to grips with economic crisis but have seen positive

growth over the last couple of years. Export volumes grew by 3.2 percent in Q1 2012 compared with the first quarter of 2011

Seafood Exports by Country

At the end of 2011, China became our leading export partner; it

was our fifth highest export partner in 2003. The large increase

in exports to China was matched by a similar decrease in exports

to hong Kong in 2011. however, hong Kong has seen a strong

start to the year with a 169 percent increase in sales compared

with the same time last year the majority of their imports have

been in rock lobster ($29m).

We have also seen the emergence of some smaller trading

partners this year, namely mauritius and Thailand while some

of the more established countries China, uS and Spain have

dropped in sales compared with the same time last year.

Exports by Species

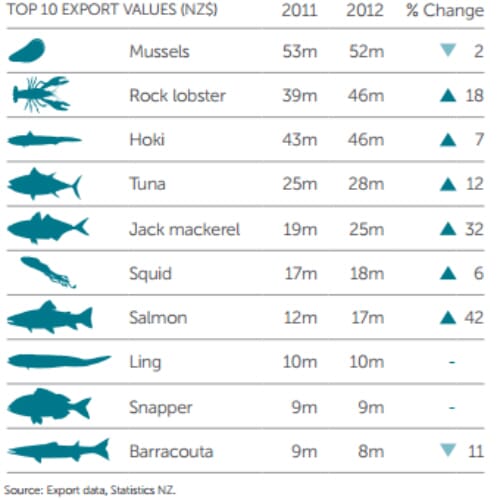

We catch more hoki than any other species, but in dollar per

kilo terms we earn more from the export of many other species

especially shellfish and crustaceans.

As catch varies significantly across the year the rankings

of these species may vary each quarter. The important

comparison is between quarters in 2011 and 2012. overall, we

saw growth in sales value of most of the top species apart from

a slight decline in mussels. ling and snapper remained stable

while barracouta dropped by 11 percent. This was due to a

significant drop in catch from five tonne to three tonne.

Exports of Main Commodities

Exports of fish, crustaceans and molluscs totalled $347m for the

first quarter of 2012, an increase of 8.7 percent compared with

same period last year. This is a positive increase given that total

exports across all merchandise fell by 1.9 percent.

As well as the $347m attributed below, the seafood industry also

exported approximately $41m in processed products such as

capsules, powders, fish cakes and fingers and other value added

products.

International Statistics

- The UN FAO reported in 2011 that the global trade in

fish and fish products set a new record with exports

reaching US$127 billion, an increase of almost 17

percent from the previous year. The main reason

is higher prices on many of the most traded fish

commodities as volumes traded only increased by 0.5

percent. Strong demand in Asia, increasing importdependency in the uS and the Eu but also buoyant

demand from many emerging markets underpinned

the rise in prices. higher prices also reflect higher in-put

costs, for example fuel and fishmeal.

- Exports for 2012 are forecast to total uS$138b, an

increase of 9.4 percent compared with 2011. despite

slow economic growth and reduced purchasing power

in many of the traditional key import markets such

as Spain, Italy and france, demand for seafood is

strong overall.

- The FAO fish Price Index suggests that fish prices will be 4 percent higher in 2012 than in 2011. rising energy and feed costs are likely to keep fish prices high during the year, especially as alternative protein sources such as meat, are influenced by the same factors.

-

fish contributes to food security in many regions of the

world. Numerous developing countries rely on fish as a

major source of protein; in 28 of them, fish accounts for

over 40 percent of animal protein intake.

- New Zealand produces less than half a percent of the worlds seafood supply, but we contribute more than double that in terms of world export dollars.

Catch Information

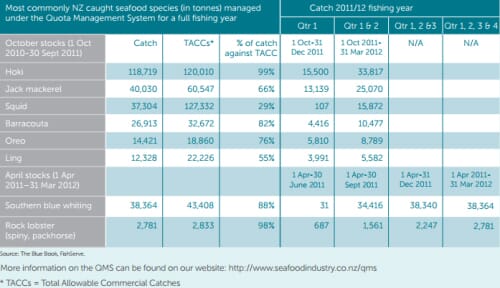

The table below shows the fish species with the largest

Total Allowable Commercial Catch limits for the october

and April fishing years. hoki has the second highest

total TACC (ie. when each species fish stock is added

together) of the october year stocks. The hoki fishery

has a seasonal peak between July and September.

Squid is a highly seasonal fishery in the late summer

and autumn (see graph opposite). It has wide naturally

occurring fluctuations in annual abundance.

other than southern blue whiting, the stocks with an

April fishing year are shellfish and crustacean stocks.

In the last full catch year, hoki and rock lobster were

caught up to their full quota limit. Species such as squid

(29 percent) and ling (55 percent) are considerably under

caught. There are several reasons why this occurs, in

addition to natural fluctuations in abundance noted

for squid. The main one being that while key target

species, such as hoki, are fully caught, the catches of

commercially valuable species associated with the

hoki fishery, such as ling and hake, are caught as a

consequence of that key target fishery and they remain

relatively under caught as a result.

The table below shows actual catch figures against Total

Allowable Commercial Catch levels (TACCs) for the

latest full fishing year (up to either April or october 2011).

The columns on the right show figures for the following

quarters up to march 2012 and will be added to in future

reports as a running record.