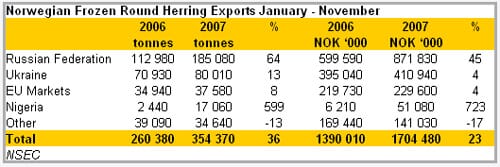

Strong autumn season in Norway

The main Norwegian herring season which began in September, has seen catch volumes up on the 2006 season. Stronger landings this year are reflected in a jump in exports with round herring volumes for the September to November period up 37%, to almost 170 000 tonnes, compared to the same period the previous year. Frozen flap and fillet export volumes are also up significantly, +50% and +34% respectively for the three month period.

|

Increased export sales from Norway have been boosted by firm demand in both the Russian Federation and the Ukraine. Together, both countries accounted for 88% of total Norwegian exports of frozen round herring for the September – November period with volume sales to these countries increasing by 44% compared to this period in 2006. For 2007 as a whole, Russia and the Ukraine are also likely to have accounted for the bulk of Norwegian exports: figures for the January – November period show a 75% share of total round exports with combined volumes to both countries up over 40%. Sales to a number of other markets have also increased with volumes to Nigeria up seven fold while increases to the EU area are more modest at 8%.

Good demand conditions this season, particularly in the Russian market, have ensured that prices have not weakened in line with increased supplies. Average export unit values for round herring for the September – November period are largely unchanged, at NOK5.04/kg, on the value for the same period in 2006. A decline is, however, evident in the frozen flap segment with average values down 10%, to NOK6.49/kg, this year.

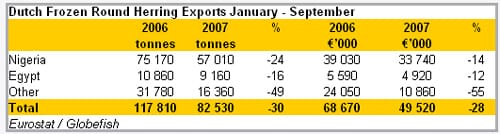

Drop in Dutch exports

In contrast to Norway, frozen round herring sales from the Netherlands for 2007 are likely to be well down on 2006 levels. Figures for the first nine months show volumes down 30%, to 83 000 tonnes, compared to the January – September period last year. The fall in exports is spread among key markets with volumes to Nigeria, the leading destination, down 24% while sales to Egypt are down 16%. In line with the Norwegian trend, average export unit values for round herring this year are largely unchanged on 2006 at €0.60/kg.

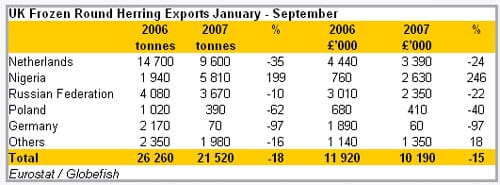

Jump in UK sales to Nigeria

The drop in frozen round exports from the Netherlands appears to have been influenced by lower Dutch imports from the UK, for re-export. UK volume exports to the Netherlands fell 35% during the first nine months of 2007 compared to the same period in 2006. With exports to the Russian Federation, Germany and Poland also down, overall UK exports of frozen round herring dropped 18% during the January September period. A notable exception to the general decline was an almost tripling of volumes to Nigeria, which became the second market, after the Netherlands, for the UK this year. As with Norwegian and Dutch exports, average unit values this year are roughly in line with those of last year at £0.47/kg.

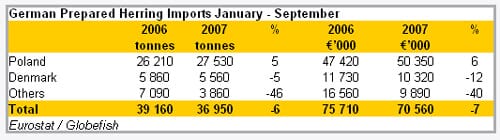

Weaker German imports

2007 looks set to have been a quieter year for German herring imports than 2006. Figures for the first nine months show a decline in all three major product categories with the chilled category showing the sharpest drop at almost 40%. The decline in imports of prepared herring products is more modest at less than 10%. The relatively strong decline in chilled imports probably reflects an ongoing shift in herring processing activity from the domestic industry to neighbouring countries such as Poland. Germany has traditionally been a significant importer of chilled and frozen herring as raw material for its marinade and canning industries. In recent years, and particularly following EU enlargement, several German companies have moved their processing activities eastwards to take advantage of more competitive cost conditions.

Despite the drop in German prepared herring imports during 2007, supplies from Poland are up on the corresponding period in 2006. This latter country appears to have been the principal beneficiary in the transfer of herring processing out of Germany. The increased German reliance on Polish supplies may also have affected imports from Denmark which are showing a slight decline for 2007. The Polish share of German processed imports is up from 67% to 75%.

Notwithstanding a drop in the EU herring quota, an almost 20% increase in the ‘spring spawning’ quota points to increased supplies for European markets for 2008. In this context, prices may be expected to weaken. There remain some uncertainties regarding the Russian market including proposed restrictions on Norwegian exporters as well as current stock levels of frozen product.