Over the past five years, the pace of decline has slowed, primarily ref lecting growth in farmed salmonids production, which partly offset continued declines in the wild-catch sector. In 2010–11, the value of Australia’s fisheries production remained largely unchanged at around A$2.18 billion, as the negative effect on prices received for export products (from the significant appreciation of the Australian dollar) was offset by higher production volumes. In 2011–12, gross value of production is forecast to rise to A$2.21 billion.

Australia’s fisheries resources and production

Historically, the majority of fisheries products were wild caught from Australia’s state, territory and Commonwealth fisheries. However, in recent years, lower wild catch volumes and the increasing efficiency and quality of aquaculture production led to a significant increase in farmed seafood products.

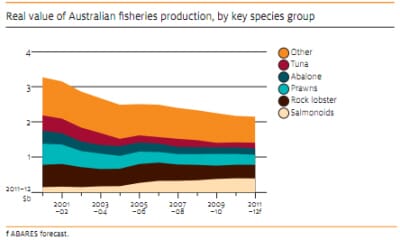

In 2009–10, Australia’s gross value of fisheries production was A$2.18 billion, one per cent lower than in 2008–09. This was the lowest gross value of production in more than a decade, having fallen by 31 per cent (A$997 million) in real terms since 2000–01. The composition of Australian fisheries production has not changed substantially over the past few years. In 2009–10 salmonids were Australia’s most valuable species group at A$369.1 million, representing 17 per cent of the gross value of fisheries production. This was followed by rock lobster (A$368.0 million, 17 per cent), prawns (A$324.1 million, 15 per cent), abalone (A$180.6 million, eight per cent) and tuna (A$125.3 million, six per cent).

Wild-catch sector

In 2000–01, the wild-catch sector accounted for around 74 per cent of Australia’s gross value of production from fisheries products. Of this, state and territory fisheries accounted for 74 per cent while the remaining 26 per cent was produced in Commonwealth fisheries. In 2009–10, the wild-catch share of Australia’s gross value of fisheries production declined to 62 per cent as a result of a fall in wild-catch gross value of production and a rise in aquaculture gross value of production.

Aquaculture sector

Despite a significant decline in the early 2000s, Australia’s aquaculture sector has grown by 18 per cent since 2004–05, reaching around A$870 million in 2009–10. As a result, the share of aquaculture production increased from 26 per cent of total value of fisheries in 2000–01 to 38 per cent in 2009–10.

The largest contributor to Australian aquaculture production is salmonids, making up 43 per cent and 42 per cent of the total aquaculture production volume and value, respectively. Between 2004–05 and 2009–10, the real value of Australian farmed salmonids production increased by 117 per cent (to A$369.1 million), supported by rapid growth in Tasmanian aquaculture production.

Australia’s trade in fisheries products

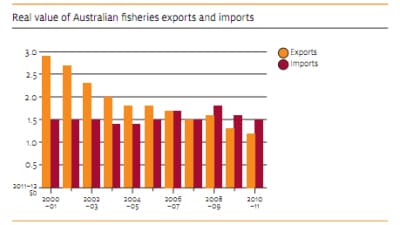

Historically, Australia was a net importer of fisheries products in volume terms but a net exporter in value terms. This is because Australian fisheries exports are dominated by high-value products such as rock lobster, tuna and abalone and imports by lower value products such as frozen fish fillets, prepared and preserved fish, and frozen prawns. In recent years, the gap between imports and exports in value terms closed and in 2007–08 Australia became a net importer of fisheries products in value terms. In 2010–11, this trend continued with the value of Australian imports of fisheries products rising by A$16.3 million (one per cent) compared with 2009–10. Australian exports of fisheries products increased by a lesser amount (A$2.1 million), further increasing the net import gap in the value of Australian fisheries product trade.

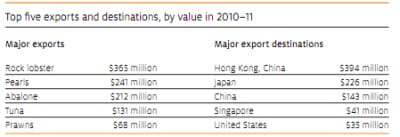

Overall, total exports of fisheries products increased by almost two per cent in 2010–11 to A$1.25 billion. Rock lobster remained the top export product with export earnings of A$365 million. The rankings of the top five exports remained unchanged between 2009–10 and 2010–11, despite an eight per cent fall in the export value of rock lobster and an 18 per cent increase in the value of prawn exports. Tuna exports increased, rising by 11 per cent, to A$131 million, while abalone fell by two per cent to A$212 million and pearls by one per cent to A$241 million.

In 2010–11, Hong Kong remained the largest destination for export of Australian fisheries products taking 41 per cent of total exports. In 2010–11, the value of exports to Hong Kong and the United States fell by 20 per cent and 28 per cent to A$394 million and A$35 million, respectively, compared with 2009–10. This was offset by a 229 per cent increase in the value of exports to China, increasing to A$143 million, while exports to Singapore and Japan rose by 10 per cent to A$41 million and five per cent to A$226 million, respectively

Outlook

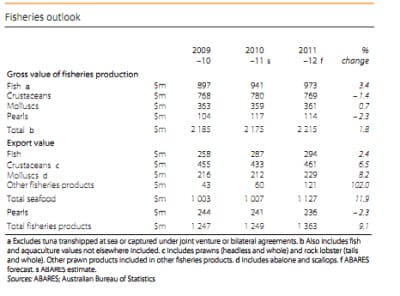

In 2010–11, Australian fisheries production was estimated to have been around A$2.18 billion, representing a 0.5 per cent decline on 2009–10. Contributing to this decline was lower production volumes of several of the higher value species, including rock lobster, tuna and pearls. In 2011–12, the value of fisheries production is forecast to increase by two per cent to A$2.21 billion. The value of tuna and oyster fishery products is forecast to rise by 18 per cent and seven per cent to A$167 million and A$102 million, respectively. These increases are expected to be offset by a five per cent fall in the value of prawns to A$294 million and a two per cent fall in the value of pearls to A$114 million.

Despite the strength of the Australian dollar against the US dollar, exports remained strong in 2010–11. Exports are forecast to increase by nine per cent in 2011–12 driven by forecast increases in scallops (42 per cent), tuna (22 per cent), rock lobster (eight per cent), and abalone (eight per cent).