Price trends

This downward trend usually reaches its bottom in November before prices increase again for the Christmas season.In the Italian market, prices of common-sized (300-450 gr) seabass and seabream declined by 4.2 percent and 7.3 percent respectively between August and September.

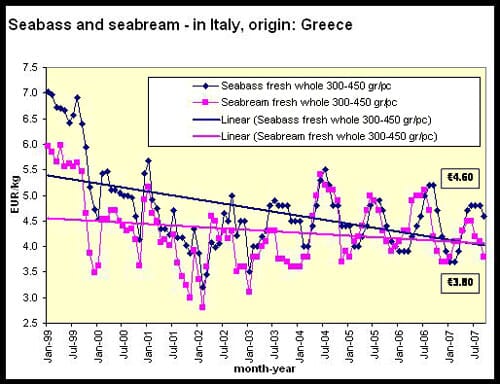

Italy – Imports growing, main exporter Greece.

In the January-May period, imports of fresh seabass and seabream into Italy increased from 11 800 tonnes, equivalent to EUR56.3 million in 2006, to 14 500 tonnes, equivalent to EUR68.9 million in 2007. Seabass import volumes increased by 30 percent and seabream import volumes increased by 15 percent. The Italian market of seabass and seabream has always been considered a mature one. In fact, the recent increase of imports can be attributed to the decline in domestic production.

Greece continues to be the main supplier of seabass and bream to Italy and the EU in general. Approximately 340 Greek farms produced 100 000 tonnes of fish in 2006, equivalent to a turnover of EUR760 million. Greek production thus accounted for over half (53 percent) of the bass and bream farmed in the Mediterranean. The output is expected to grow in the coming years (see News section).

Italian imports from Turkey are increasing considerably. Turkish farms are currently estimated to produce approximately 30 000 tonnes/year of either species. However, at the moment, several fish farms are being moved away from the coast, into the open sea, in order to implement a governmental regulation of January 2007. The regulation was motivated by concerns over the industry’s wastes and by aesthetic reasons. This relocation of the farms may result in lower production and declining exports from Turkey into Italy and other EU countries.

Spain – Domestic farm capacity still under expansion.

Spanish imports increased by 15 percent in January-May 2007 compared with the same period of the previous year, mainly due to higher seabass imports. Imports of this species now represent more than 60 percent of total imports of fresh seabass and seabream. Spanish imports of European seabass increased from 3 300 tonnes in January-May 2006 to 4 400 tonnes in the corresponding period in 2007. In turn, imports of seabream (S. aurata, but also Dentex dentex and Pagellus spp.) declined slightly from 2 800 tonnes in January-May 2006 to 2 600 tonnes in the same period in 2007. Greece remains the main country of origin, but consumption of domestically-produced fish is expected to grow due to recent investments aimed at enhancing farming capacity in the country (see News section).

France – Imports of Dentex dentex and Pagellus spp. declining.

French imports of seabass and seabream declined from 3 000 tonnes, equivalent to EUR12 million, in the first semester of 2006, to 2 600 tonnes, equivalent to EUR11.8 million, in the first semester of 2007. Imports of European seabass D. labrax increased by 3 percent and imports of gilthed seabream S. aurata declined by 2 percent. The most relevant decline concerned breams nei (namely D. dentex and Pagellus spp.), whose imports dropped by 31 percent in volume and 22 percent in value between the first semester of 2006 and the first semester of 2007. This decline affected supplies from countries which are outside the traditional bream farming circuit, e.g. the United Kingdom.

Outlook

The trend of fresh seabass and seabream imports into the main EU markets seem to have changed slightly in the first five to six months of 2007. In fact, the general trend was for the French market to be more vibrant as opposed to the Spanish and, in particular, the Italian market. In January-May 2007, however, Italian and Spanish import volumes of fresh seabass and seabream increased by 23 and 15 percent respectively compared with the same period in 2006. In contrast, French import volumes of fresh seabass and seabream declined by 7 percent in the first semester of 2007 compared with the same period in 2006.

In Italy, the declining supplies of domestic fish are the main reason behind the increase in imports of foreign fish, and therefore further increases are likely in the future. In the Italian market, seabass and seabream are often used in sales promotions in supermarkets, and thus the market has a continuous need for steady and cheap supply. In Spain, it will be interesting to follow the evolution of the market share of domestic production as opposed to the share of imported products. In France, the current situation seems to be due to a temporary market adjustment, rather than the indication of a new trend.

Despite showing a declining pattern since 1999, prices of farmed seabass and seabream are also cyclical. At present, farmers are in a situation of excess supply, therefore they are lowering price offers in order to get rid of the old generation fish and make room for the new generation fish next year. The price decline is expected to reach a low between late November and early December. However, at that point, supplies of the old generation fish would have become scarcer and the imminent Christmas festivities would push demand up. Lower supply and higher demand are therefore expected to generate price increases. From January onwards, seabass and seabream supplies would become even scarcer as the new generation fish would have not reached the marketable size of 350-400 gr before July. Prices are therefore projected to increase, and even more so during late spring and the early summer when demand for fish is higher in Mediterranean Europe. Price would start softening once again in August, further to the full availability of market size fish.

News

Spain: expanding production capacity

Norwegian aquaculture group Marine Farms ASA said on 11 June 2007 that Piagua, a subsidiary of Marine Farm's Spanish business Culmarex SA, has received approval to increase its annual capacity from 1 500 tonnes to 2 500 tonnes. Following the capacity expansion Piagua will be the biggest seabass/seabream site in Spain.

Marine Farms ASA said on 6 August 2007 that its Spanish arm Culmarex SA is expanding its operations through the acquisition of the assets, concession and fish stock of CIM Delta del Vinalopo. The purchase price is approximately EUR 2.8 million. Culmarex is carrying out the transaction through its wholly-owned subsidiary Granja Marina Bahia de Santa Pola SAU (Gramabasa), a neighbour of Delta del Vinalopo. Both companies are located in Santa Pola Bay in Spain's Alicante province. Delta del Vinalopo is currently awaiting an increase in concession capacity to 1 200 tonnes of seabass and seabream per year.

Greece: Selonda taking over European seabass and seabream production

Greece-based aquaculture producer Selonda wants to control at least half the production of all seabass and seabream in Europe and Turkey within the next five years. The company is now Greece’s second largest farmed fish producer, responsible for every fifth bass and bream in the country. The company is already on track to achieving its goal after acquiring a 46% stake in Fjord Marin Turkey, while the remaining 54% is owned by the Norwegian company Fjord Marin AS. The two companies produce around 35 000 tonnes of bass and bream. In Greece, six companies account for around 80% of production. More than 300 companies share the remainder.