Markets and Prices

Prices of fish and fish products are generally under downward pressure, as falling consumer demand is hurting seafood sales in all markets. The only species that have spared the price fall are those that have experienced problems that have constrained output.

They include some wild whitefish species and yellow-fin tuna but also farmed salmon and tilapia, the prices of which remain firm. Other farmed species such as European seabream and turbot have seen prices falling to record-low levels, due to large increases in production. On the other hand, catfish prices in Viet Nam, which tumbled earlier this year, are now recovering. Shrimp prices remain low.

International shrimp prices, which were already depressed before the financial crisis, are most likely to weaken further in the course of the year, as import demand is expected to slow down in all main markets. The European Union, which until recently was an exception to otherwise depressed shrimp markets in Japan and the Unites States, is now also showing signs of weakness, with the volume of shrimp imports down 10 percent to 337 600 tonnes in the first half of 2008. Only France increased its purchases, whereas Spain and Italy registered massive drops.

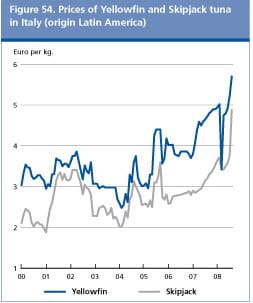

Voluntary fishing bans by the Ecuadorian and Japanese fleet have contributed towards reduced supply and record prices on many tunaspecies including yellow fin. In early September 2008, the catches of skipjack in the Indian Ocean improved significantly pushing it’s price down to EUR1 120/tonne. Meanwhile, the price of cooked and frozen tuna loins in Europe continued to increase due to the increasing cost of raw material in Ecuador.

Squid prices remain low, due to limited buying interest in Japan and the rush by Argentine squid fishing fleet to sell at discounted prices. This situation is expected to persist until early 2009, when the new fishing season in the Southwest Atlantic starts. By that time, inventories dating back to 2007 will have reached the market and buying interest is expected to recover strongly.

The world octopus market was characterized by ample supply in the second and third quarter of 2008, with prices declining somewhat. However, with demand in all main markets strengthening, prices of octopus are likely to go up somewhat in coming months. In Japan, New Year’s festivities are generally an excellent sale period for octopus, while in Europe demand for octopus is strongest in summer months.

The overall situation in the European bass and bream market is mixed at the moment: bream prices are extremely weak, giving producers a reason for concern. Bass prices, on the other hand, are holding up well, resulting in a record price differential between the two species. In the next few months, demand is expected to remain weak, but it may strengthen again before Christmas. The cyclical nature of production is likely to reduce supply during the winter months, which may underpin prices for both species.

The market for farmed salmon has been remarkably stable, partly as a result of supply problems in Chile. Prices, although lower than in 2007, are still remunerative for most producers and could start to rise up until early next year, reflecting the effect of Chile’s reduced production on global supplies.

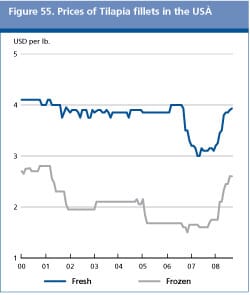

After severe production problems in 2007 and early 2008, tilapia prices have skyrocketed, making tilapia production attractive also for new producers, including many companies now suffering from low shrimp prices. Increased output from both China and other producers is therefore likely to boost availabilities and bring prices down to more normal levels in 2009.

Strong price increases are reported for catfish as processors are rushing to meet increasing demand from Russia, Ukraine, East Europe and countries in the Near East, resulting in a more than doubling of exports from Viet Nam in the first half of 2008.

The main fishmeal importer, China, has returned to the market in 2008 with strong buying interest, leading to relatively high prices in the second quarter. In the third quarter fishmeal prices trended downward, but much less than soybean meal. In September 2008, fishmeal was priced at USD1190/tonne, about USD150/tonne more than in September 2007 and only USD50/tonne below the July2008 peak. Some downward movements in prices may be expected in the coming months, although much will depend on the fishing quotas that still have to be set in Peru. If kept at 2million tonnes, as expected, prices could fall, given the reluctance of the European market to purchase at the present price levels and the expected slow down of demand in China, which is currently holding large stocks.

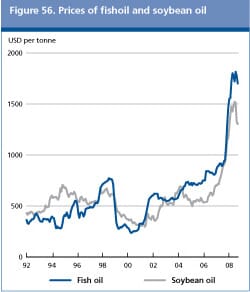

Fish oil prices reached an all time high of USD1 815/ tonne in July 2008, but since then they have started to soften, in line with vegetable oil prices. Demand from the fish oil capsule industry was extremely low in the third quarter of 2008, in anticipation of the tougher European Union norms. The present market situation points towards a decline in fish oil prices in the coming months, as buyers appear well covered, producers have large stocks and the prices of the competing vegetable oil prices are weakening. In addition, the new season in Peru is likely to add substantial quantities of fish oil to the market.

Major revision to 2006 production statistics by China

China has reported that it is in the process of revizing its fishery and aquaculture production statistics downwards, based on the outcome of the National Agricultural Census of 2006, which, for the first time, covered fisheries and aquaculture sectors. Revised statistics are expected to be released in 2009, which will be reflected in FAO statistics. In Food Outlook, Tables 11 and Table A20 (in the Statistical Appendix) include preliminary figures received from China for 2006. Following this revision, world capture and world aquaculture fishery productions in 2006 are now 2.4 million tonnes and 3.3 million tonnes lower than previously reported, respectively.

Production

In 2008, global production of fish and fishery products, from either capture or aquaculture, is expected to increase by 1percent only, from the level in 2007. The increase is expected to reflect gains in aquaculture, more than compensating for a contraction of capture fish. Aquaculture is forecast to continue to grow in 2008, largely to meet growing demand. However, growth may be dampened next year by low market prices of several species, as well as high fuel and feed costs, which are forcing many producers to reduce production in the short term. In addition, supply problems related to disease and bad weather have had a negative impact on salmon production in Chile and on tilapia in China. On the other hand, capture fish production is forecast to end slightly down compared with 2007, partly as a consequence of higher fuel prices, which provided strong incentives for the fleet to curb the less profitable operations, but also due to the resource situation, which is critical for many species.

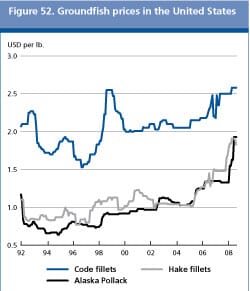

With shrimp prices weak and demand falling, shrimp production from both wild and farmed sources is expected to contract, as many Asian and South/Central American producers are reducing output. Thailand, for example, forecasts lower harvests of vannamei shrimps, reflecting a shift by farmers towards more profitable black tiger shrimp, as well as tilapia. Production of tuna is also likely to fall, as many to the main producers are cutting fishing operations, including the Chinese Province of Taiwan, Ecuador and Japan. There, the Japan Tuna Fisheries Cooperative Association (Tuna Japan) decided to suspend fishing operations of all its 233 member vessels, effective 1August2008. The duration of the suspension will run from two months to two years, depending on each vessel’s fishing plan. World production of cod and hake is expected to diminish this year, constrained by the reduced groundfish stocks. At present, quotas for Alaska pollack are in free fall, while many cod resources are overexploited, with catches declining sharply during the past decade. Argentine landings of hake were also down in the first half of 2008 (minus 4percent). Southern Africa seems to be an exception, with hake resources apparently in good shape. By contrast, the world octopus production has been increasing in the second and third quarter of the year. Moroccan management schemes have been successful in rebuilding resources. As a result, larger octopus catches have been allowed. Heavy landings of Illex squid at the start of the season led to very low squid prices, which together with high fuel prices, made fishing uneconomical. As a result, production is set to fall in the course of the year.

Production of farmed European bream is on the increase in major producing countries, such as Greece and Turkey, while bass production is reportedly stable. As a result, prices of bass has been holding much better than bream prices. The large price differential is giving important signals to producers, which could induce a shift towards bass in 2009. Finally, although production is still limited, a new species, “meagre”, has been expanding. Meagre has significant market potential because of its excellent texture and taste, but demand still needs to be built up through consumer information and communication campaigns. Production of farmed salmon may fall, as problems in Chile have led farmers to harvest the fish early, resulting in much lower yields. Norwegian companies have also started experiencing production problems. In China, tilapia producers experienced severe losses during the cold 2007-2008 winter. Depressed catfish prices in late 2007 and early 2008 led to reduced production and supply, resulting in a strong rebounding of prices in the course of 2008. In response, producers are now gearing up production volumes again. A strong expansion is expected in Viet Nam, which plans to step up production, to meet the industry’s objective to reach an export value of USD1.5 billion in 2009.

In the third quarter of the year, fishmeal production was characterized by limited catches, a normal feature for this period of the year. However, production over the full 2008 now looks set to decline, in contrast with 2007, when the market was characterized by over-supply and declining prices. Indeed, European producers are getting close to the end of the fishing season, while in the Pacific area, production is currently suspended. In Peru, the fishmeal producers are awaiting new research data, the basis for the quota of next season this November and December. All observers anticipate the fishing quota to be maintained at last year’s level of 2million tonnes. Fish oil production mirrored that of fishmeal with output declining in 2008. In the first half of the year, 332 000 tonnes were produced by the top five producing countries, a 20percent drop from the corresponding period of 2007.

Prospects for fish production in 2009 now point to limited growth, as a weakening demand may depress prices. Higher financing costs are also likely to have a negative impact especially on carnivorous aquaculture production, as many producers are responding by curtailing output. Nonetheless production from aquaculture is still anticipated to increase as freshwater and herbivorous species dominate the sector.

Financial crisis and the fishery sector

Turbulence in world financial markets is being transmitted to the fishery sector. Credit is getting scarce and margins, which already are comparatively low in this industry, are getting thinner. Export finance is also becoming more difficult to obtain with banks tightening up the conditions for issuance of letters of credit. With almost 40 percent of all fish produced, whether from capture or aquaculture, now entering international trade, this could have a drastic effect on trade over the next months.

Likewise, the difficulties of many banks heavily involved in the financing of world capture fisheries and aquaculture development, such as the three Icelandic banks now taken over by the Icelandic state, are also limiting credit availability to the sector. Contrary to the fuel crises, which hit the capture sector particularly hard, the ongoing credit crunch is having a severe impact also on the aquaculture industry, and especially on the farmers producing carnivorous species, which are heavily dependent upon industrial feed. For these species, the production cycle typically lasts a couple of years before the fish reaches market size, making feed and finance the largest cost factors in production. On the demand side, consumers are reducing their discretionary spending and the decline in restaurants visits is hurting the fishery sector.

Trade

Global trade in fish products is forecast to reach 54.5million tonnes in 2008, marginally below the previous year’s estimate.

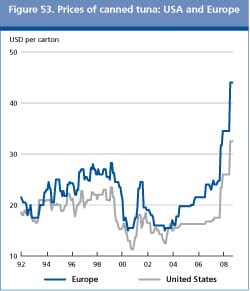

Shrimp trade volumes are expected to fall over the next quarters, as poor demand prospects are encouraging importers to cut back imports and to draw, instead, from their frozen inventories. At the same time, tighter trade finance and export credits are encouraging producers and exporters to lean more on domestic markets. Despite poor domestic demand and increased landing prices in the sashimi tuna market, Japan’s imports of tuna, including loins, increased by 4percent in January-June 2008, against the same period last year, but the growth may not be sustained. The United States’ tuna market was negatively affected by weak demand for canned tuna and tuna pouches. The European Union import demand is also forecast to be depressed by rising prices of raw material. With weakening import demand in the three major markets, exports from Thailand, the largest canned producer, may decline, which is prompting the country to actively look for new markets in the Near East and in Mexico.

During the first half of 2008, imports of groundfish by the United States fell by 9percent, largely reflecting reduced purchases of both fillets and blocks, a situation likely to also prevail over the rest of the year. The United States usually exports Alaska pollack to China for processing and subsequently re-imports the processed product this year. Lower United States catches of Alaska pollack limited availability of raw material for the Chinese filleting and processing industry for re-export. Similarly, supplies from Northern Europe to China for processing was reported to face difficulty in securing adequate trade finance for exports. This could contribute to lower the volume of groundfish trade in the next couple of quarters.

By contrast, all the major import markets of octopus have reported increases in deliveries so far this year. Japan imports in the first half of 2008 were up 15percent, while those by Italy, traditionally the second major octopus market, rose by 12percent. Spain, also a significant market, increased January-June imports by 20percent. On the export side, Viet Nam is consolidating its position as a major octopus exporter. The country has managed to enter the Italian baby octopus market, a product mainly utilized in the processing industry of marine salads, where it represents a convenient alternative to cuttlefish. Squid imports by Spain, the major market in Europe, reported record imports during the first half of 2008.However, squid purchases by Italy and Japan are likely to decline in 2008. The two countries are holding large supplies, as both stepped up their imports in 2007, when international prices were particularly low. Squid exports from Peru and the United States are forecast to expand, while a sharp decline in Indian and Peruvian catches may affect negatively their shipments.

Imports of farmed salmon in 2008 have held up remarkably well, especially in the European Union and Japan, but also in several Latin American countries. Purchases by the United States showed some weakness in the first half of 2008. World demand is still good for this species although supply problems in Chile could cause somewhat higher prices next year.

Similarly, trade in tilapia is expected to increase in 2008, despite a slowdown in the second quarter of the year. Much of the expected expansion would be on account of larger purchases by Mexico and the Russian Federation, which would compensate for reduced deliveries to the United States. The brisk world demand is anticipated to sustain deliveries from non-traditional exporters in Latin America, as supply problems in China, arising from damage to the tilapia production centres incurred last winter, will limit the country’s ability step up its exports.

Trade in catfish could also be boosted byincreasing demand from the Russian Federation, Ukraine and countries in the near East. Imports by the United States and countries in the European Union, in particular Spain, are also expected to grow. The strong import demand is expected to boost exports by Viet Nam to a new record level.

Trade in fishmeal, on the other hand, may be constrained this year by a poor import demand by both China and the European Union. Imports to Germany, in particular, were 30percent less over the first half of the year than in the same period of 2007. The decline in world import demand is likely to affect mostly deliveries from Peru. Weaker prices for several farmed species may also soften import demand in fish oil, much of which is used as a feed component in the aquaculture industry.

| World fish market at a glance | ||||

|

2006

|

2007

|

2008

|

Change: 2008 over

|

|

|---|---|---|---|---|

|

|

|

|

estim.

|

2007

|

|

|

million tonnes

|

%

|

||

|

WORLD BALANCE

|

|

|

|

|

|

Production

|

138.0

|

142.6

|

144.2

|

1.1

|

|

Capture fisheries

|

89.6

|

91.8

|

91.0

|

-0.8

|

|

Aquaculture

|

48.4

|

50.8

|

53.2

|

4.7

|

|

Trade value (exports billion USD)

|

85.9

|

92.7

|

98.8

|

6.6

|

|

Trade volume (live weight)

|

53.5

|

55.0

|

54.5

|

-0.9

|

|

|

|

|

|

|

|

Total utilization

|

|

|

|

|

|

Food

|

110.4

|

112.3

|

114.5

|

1.9

|

|

Feed

|

20.9

|

20.8

|

20.0

|

-3.8

|

|

Other uses

|

6.7

|

9.5

|

9.7

|

2.6

|

|

|

|

|

|

|

|

SUPPLY AND DEMAND INDICATORS

|

|

|

|

|

|

Per caput food consumption:

|

|

|

|

|

|

Food fish (kg/year)

|

16.7

|

16.8

|

17.0

|

0.7

|

|

From capture fisheries (kg/year)

|

9.4

|

9.2

|

9.1

|

-1.5

|

|

From aquaculture (kg/year)

|

7.3

|

7.6

|

7.9

|

3.4

|

Utilization

Total fish utilization is expected to increase, sustained by a 2 percent anticipated expansion in food consumption, which is forecast to reach 115 million tonnes in 2008. As a result, per caput fish consumption is estimated to hover around 17 kg in 2008, up from 16.8 kg in 2007. By contrast, utilization as feed is set to decline by almost 4 percent to 20 million tonnes, driven by a contraction in fishmeal production.

With credit becoming a problem for many operators, trade volumes and utilization could suffer with declining imports. This may result in stagnating fish consumption in several of the major markets that rely on imports to meet their needs. Stagnating or falling incomes may induce some consumers to reduce their fish intake and/or to shift towards cheaper fish products. The shift towards cheaper fish alternatives would negatively affect the higher priced products, in particular shrimps. Consumers may also respond to changes in relative prices by turning towards farmed fish species, in particular, Vietnamese catfish, European seabream and farmed salmon.

Following the downward revision of Chinese production statistics, world estimates of consumption have also been adjusted downward. As a result and contrary to the previous conclusion, aquaculture has not yet overtaken capture fish as a source of fish for human consumption. However, this possibility cannot be ruled out to materialise in the near future, given current prospects for strong growth in aquaculture.

November 2008