This is just another indication of the current status of the US economy, but, how much this can effectively affect shrimp consumption, is not very clear. Traditionally, shrimp is considered an upper-end product, and economic crisis in the USA have always resulted in lower shrimp consumption. However, some recent reports indicate that shrimp might be less affected by the present crisis than other food product.

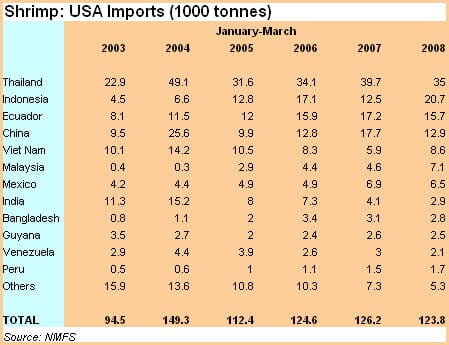

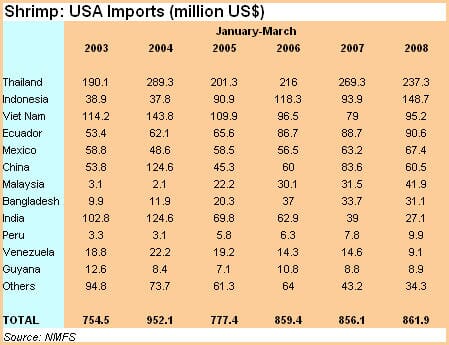

US imports of shrimp in the first quarter of 2008 totalled 123 800 tonnes worth US$ 862 million. These figures show a small reduction in quantity (-2%), while the value of imports remained almost unchanged (+0.7%), compared to the same period in 2007. Monthly shrimp imports in the USA are generally slow until May, after which they start to recover, just before the offset of summer.

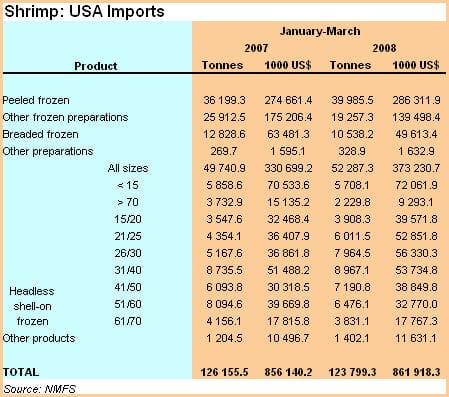

In the first quarter of 2008, the main imported product was headless shell-on frozen shrimp, with 52 300 tonnes accounting for 42% of total imports. This category reported a 5% growth compared with the same period of 2007. The unit value of this product grew by 7%, and as a result, total value of imports of this category rose by 13% reaching US$ 373 million.

The second most imported product during the period under review was peeled frozen shrimp, which accounted for 32% of total foreign supply of shrimp (40 000 tonnes worth US$ 286 million). Compared to the first quarter of 2007 sales of this product to the US grew by 11% in terms of volume and by 4% in terms of value. Breaded frozen shrimp and other frozen preparations continued to show the decreasing trend already experienced in 2007, and imports fell for both categories.

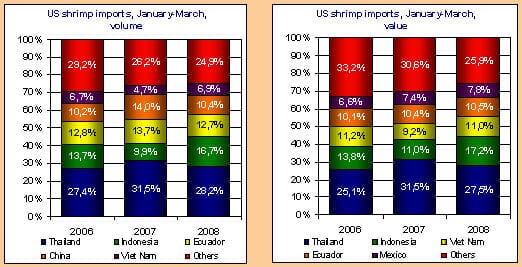

Thailand remained the leading supplier of shrimp to the US market with 35 000 tonnes in the first three months of 2008, representing 28% of the total volume. Sales from this country fell by 12% (both in volume and value). Indonesia was the second main supplier, with 20 700 tonnes and a remarkable growth in sales, both in volume and value. It is interesting to note that in terms of volume, the third supplier was Ecuador, with 15 700 tonnes, while in terms of value, the third exporter to the US was Viet Nam (US$ 95 million). Probably the main reason for this difference is due to Ecuadorian sales which are mainly frozen shell-on while 46% of total Vietnamese sales are peeled frozen shrimp, which have a higher unit value.

Chinese sales have not recovered from the problems suffered during 2007, and registered once more a reduction in trade. Sales in the first quarter of 2008 from this country were 27% and 28% lower both in terms of volume and value (12 900 tonnes; U$S 60.5 million). China remained the top supplier of breaded frozen shrimp, with 62% of total imports, however, sales of this product fell significantly (-37%), and Thailand managed to seize this market window. Sales from this nation grew by 53% in the period reviewed.

Asian nations accounted for almost 80% of the total supply of peeled frozen and for over 95% of other frozen preparations and breaded frozen to the US market, while frozen shell-on shrimp has a higher share of Latin American supplies.

July 2008