Overview

The Irish seafood industry makes a significant contribution to the national economy in terms of output, employment and exports. Generating approximately 11,000 jobs1 in rural coastal regions, it is estimated that the industry contributed approximately €750 million to the national economy in 20062.

Geographically the fisheries industry is predominantly concentrated on the western seaboard and the harbour towns of the south and east coastline areas. In terms of the fish catching sector, fish and shellfish are landed at the five major Fishery Harbour Centres (Killybegs, Castletownbere, Howth, Rossaveal, and Dunmore East), at 40 secondary ports (each with landings exceeding €1m) and a further 80 piers and landing places where fish landings are recorded3. The main industry stakeholders are the primary production sectors of fish catching and aquaculture, the primary and secondary processing sectors, the marketing sectors and ancillary industries such as net making, vessel repair, transport, and a number of other services.

While consumer demand for seafood is growing strongly, as illustrated by the growth in the sales value of Irish seafood from €617 million in 2000 to approximately €750 million in 2006, the supply of seafood is facing difficulties mainly due to the declines in fish stocks, declining quotas and structural imbalances at catching and processing levels.

Fleet Size and Structure

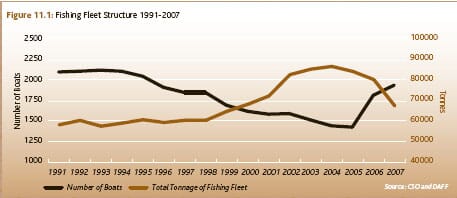

Figure 11.1 illustrates trends in the size and structure of the fleet since 1991. In 20074 the Irish fishing fleet consisted of 1,935 vessels with a total tonnage of 64,489 tonnes and a total engine power of 201,605 KW.

The sharp increase in the number of registered ships since 2005 can be attributed to an increase in the Polyvalent Segment of the fleet. This was due to 490 vessels being licensed and registered under the Special Scheme for the Licensing and Registration of Traditional Pot Fishing Boats. The removal from the Fishing Boat Register of the MFV5 “Atlantic Dawn” during 2007 resulted in a significant reduction in Registered Fleet Capacity of 14,055 tonnes and 12,607 KW.

The Irish fleet contains 5 main segments:

- Refrigerated Seawater (RSW) Pelagic Segment: This segment is engaged predominantly in fishing for pelagic species (herring, mackerel, horse mackerel and blue whiting mainly).

- Beam Trawler Segment: This contains vessels, dedicated to beam trawling, a simple trawling method used predominantly in Irish inshore waters except in the southeast, where it is used to catch flatfish such as sole and plaice.

- Polyvalent Segment: This segment contains vast majority of the fleet. These vessels are multipurpose and include small inshore vessels (netters and potters), and medium and large offshore vessels targeting whitefish, pelagic fish and bivalve molluscs.

- Specific Segment: This segment contains vessels which are permitted to fish for bivalve molluscs and aquaculture species.

- Aquaculture Segment: These vessels must be exclusively used in the management, development and servicing of aquaculture areas and can collect spat from wild mussel stocks as part of a service to aquaculture installations.

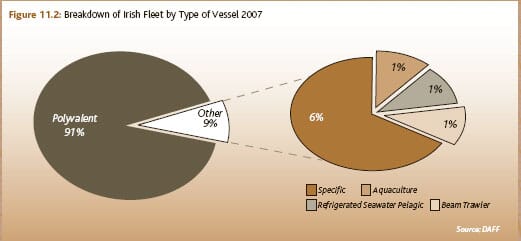

The vast majority of the fleet are within the polyvalent segment, which comprised 1,737 vessels in 2007. A breakdown of the fleet by type of vessel is outlined in Figure 11.2

Primary Production from Fisheries

Landings

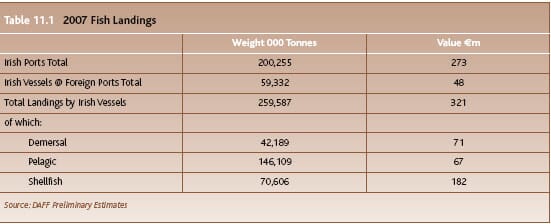

Data on 2007 landings by broad species type6 is outlined in Table 11.1. The volume and value of fish landed by Irish vessels in 2007 amounted to almost 260,000 tonnes worth approximately €320 million. In volume terms, approximately 55% of landings were comprised of pelagic species with a value of almost €67 million. Landings of shellfish accounted for less than one-quarter of total landings in terms of tonnage, but accounted for over half (57%) of the value of total landings (€182 million approx). Demersal landings accounted for over 42,000 tonnes valued at over €70 million.

Aquaculture

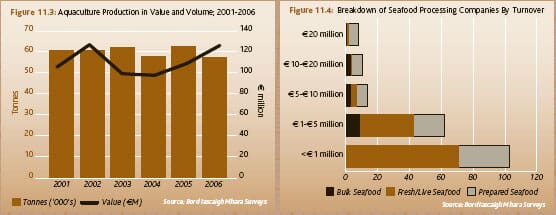

Aquaculture activities are located right around the coast with particular concentrations in Donegal, Connemara, West Cork, Waterford, Wexford and Carlingford Lough. The sector includes the farming of finfish species such as salmon and trout, artic char and perch. Shellfish species such as mussels and oysters are also farmed extensively. Aquaculture derived seafood products have the potential to fill the gap between supply and demand for fish produce, given that output from traditional capture fishery is constrained by terms and conditions and quotas at EU and international level. In 2006, it is estimated that the aquaculture sector accounted for approximately 20% of the volume of total primary production of fish and shellfish. This was valued at over €124 million7 in 2006. Aquaculture production in terms of value and volume between 2001 and 2006 is outlined in Figure 11.3

Seafood Market and Processing Sector

Irish seafood sales on home and export markets8 were valued at €724.6 million in 2006, an increase of 9% on 2005 (€665 million)9. Within the domestic market sales grew 17% to €362.4 million. When landings by Irish vessels at foreign ports (approximately €26 million10) are included this brings the total value of seafood sales in 2006 to approximately €750 million.

The Seafood Processing Sector

The seafood processing sector is concentrated in the coastal regions of Donegal, Galway, Cork, Kerry and the South East. There are approximately 200 firms, mainly SMEs, engaged in handling, distribution and processing of fish. Less than 5% of these companies had more than 50 people employed full-time, while a significant number of small operators supply a local market or sell to niche market outlets.

Figure 11.4 provides a breakdown of the seafood-processing sector (based on BIM surveys in 2005) by level of turnover. The graphic illustrates the lack of economies-of-scale within the industry. Less than 10% of all companies operate with annual turnovers in excess of €10 million, with the top 50 companies accounting for 80% of overall turnover in the sector.

Exports

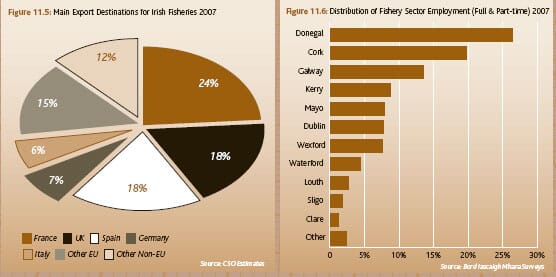

CSO data estimates that Irish seafood exports were €352 million in 2007, a slight increase on 2006. Approximately 87% of seafood exports were directed to EU markets with the balance going mainly to Far Eastern and African markets. The main market destinations have remained largely unchanged over the years with France being the premier market accounting for approximately one-quarter of exports with a value of over €86 million in 2007. This was followed by Great Britain at a value of €64.4 million and Spain €63.1 million. The main export destinations are outlined in Figure 11.5.

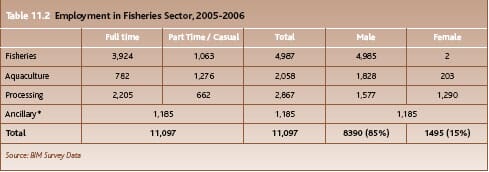

Employment in the Fisheries Sector

The seafood industry supports the economic viability of many coastal communities, directly generating or supporting approximately 11,097 jobs11. This includes full and part time/casual employment in the fisheries, aquaculture, seafood processing and ancillary services sectors. Table 11.2 gives a breakdown. Figure 11.6 below gives the distribution of employment throughout the country in the overall fisheries sector.

Footnotes

Based on BIM surveys, which include full and part time/casual employment in the fisheries, aquaculture, seafood processing and ancillary services sectors. This is not comparable to CSO QNHS data quoted elsewhere in this report. Latest year for which complete data is available. Includes seafood sales, exports and landings at foreign ports. National Seafood Strategy Report "Cawley Report", January 2007. On 31/12/2007. Source: DAFF Motor Fishing Vehicle Main species grouping and most important species contributing to landings Pelagic: Mackerel, Horse mackerel, Herring, Sprat, Sardines Demersal: Cod, Saithe, Haddock, Whiting, Hake, Megrim, Monkfish, Ling Shellfish: Nephrops, Scallops, Mussels, Crabs, Lobsters, Squid, Cuttlefish Status of Irish Aquaculture Report 2006. The figures quoted here are exclusive of the value of landings by Irish Vessels at foreign ports. BIM Annual Report 2006. DAFF Estimate.Further Reading

| - | You can view the full report by clicking here. |

July 2008