China consolidates position in frozen cod fillet markets

Globalization in the seafood industry continues to be well illustrated in the frozen groundfish sector with Atlantic cod caught and frozen in European fishing zones, exported to Asia where it is filleted and re-exported back to Europe for sale in frozen fillet markets.

|

China, where the bulk of the filleting activity takes place outside of Europe, is now the top supplier to European markets such as the UK, Germany and France and has expanded market share at the expense of north and east European producers who find it difficult to compete with the lower costs enjoyed by Chinese processors.

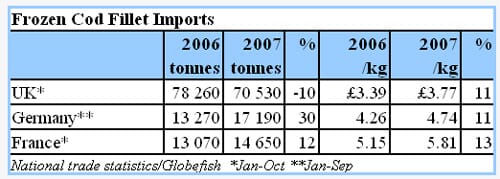

Partial figures for 2006 and 2007 suggest that the process is ongoing with China increasing its share of frozen fillet imports of cod (both Atlantic and Pacific species) in key markets last year. The Chinese gains come in a context of falling catch levels and increasing raw material costs. Lower landings are reflected in a 10% drop in import volumes in Europe’s largest cod market, the UK, while higher cod prices are reflected in increased average import values in several European markets.

Weaker UK imports

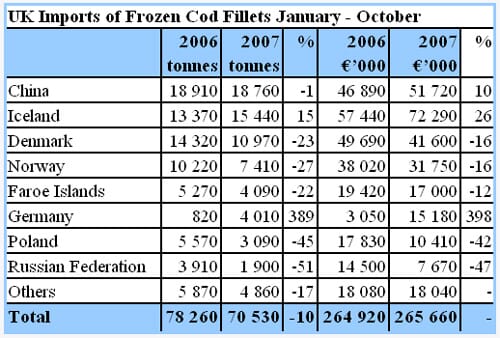

Among the major frozen cod suppliers to the UK market during the first ten months of 2007, only Iceland and Germany managed to increase volume sales compared with the same period the previous year. Germany showed the strongest increase, volumes jumping five fold to 4 000 tonnes. With limited domestic cod landings in Germany, this sharp increase in German supplies to the UK is likely to consist of re-exports of imported product, possibly of Chinese origin - as noted below, Chinese sales to Germany increased significantly during 2007.

For the UK market, direct sales from China were stable last year with volumes for January – October marginally down on the first ten months of the previous year. Despite this slight decline, China’s share of UK imports increased, up from just under a quarter for 2006 to almost 27% in 2007. In value terms, China’s share of imports increased from less than 18% to almost 20%. This increase allowed China to overtake Denmark as the second supplier while Iceland remains the top supplier to the UK in value terms.

In contrast to the increasing import shares of Iceland, Germany and China is the drop in shares of traditional cod fillet supplying countries to the UK such as Denmark, Norway, the Faroe Islands and the Russian Federation. In absolute terms, the sharpest decline in supplies to the UK last year concerned Denmark which saw fillet sales drop by almost 3 500 tonnes for the ten month period. This decline partly reflects a switch by Danish suppliers from the UK to the German market – as noted below, Danish volume sales to Germany almost doubled last year. In percentage terms, supplies from Russia suffered the biggest decline with volumes more than halving to less than 2 000 tonnes.

The increase in cod fillet import prices is reflected in higher average unit values for all major suppliers to the UK market with increases of between 9 and 15%. The overall average for total imports is up 11% compared to 2006 to £3.77/kg.

Jump in supplies to Germany

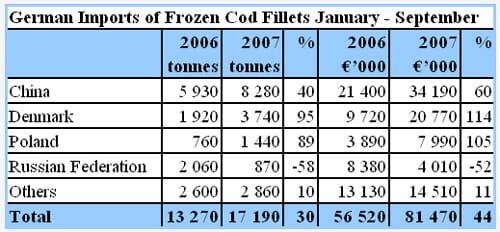

The negative trend in Russian supplies is also evident in the German market where Russian volumes dropped by almost 60% during the January – September period last year. The decline in Russian fillet sales to both Germany and the UK suggests that Russian cod producers are oriented less towards fillets and more towards whole / h&g supplies for Chinese processors. For the German market, Russia’s share of imports is down to 5% from over 15% the previous year. In contrast, Chinese volume sales to Germany increased by 40% last year with the Chinese share of imports touching the 50% mark as a result. The increase consolidates China’s position as the top supplier in both volume and value terms.

As in the UK, import unit values increased for all major suppliers to the German market last year. The range of increases was similar to the UK, between 9 and 14% with the overall average at 11% to €4.74/kg.

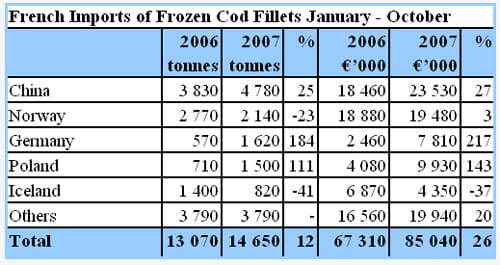

China top supplier to France in volume and value terms

Following a 27% increase in sales to France during 2007 (10 months), China passed Norway as the leading supplier to this market in value terms. China also consolidated its top position in volume terms following a 25% increase while French imports from Norway, the second supplier, declined by a similar percentage. As in the UK, German supplies to the market jumped last year, almost tripling compared to the January – October period in 2006. Also up significantly were French imports from Poland, more than doubling compared to the previous year.

Positive price outlook

No significant improvement in European cod landings is likely during 2008 and, with other groundfish fisheries, such as the US pollock fishery, expected to be lower, upward pressure on cod fillet prices look set to continue into the second half of the year.

January 2008