Report Highlights:

Total aquatic trade value is also expected to increase rapidly to an estimated $21.7 billion. US aquatic exports to China increased 58 per cent to $930 million in the first ten months of 2011 but still face an aquatic trade deficit exceeding $1.1 billion. Prospects remain strong for frozen fish, including salmon and plaice. Reduced import duties for several fish products in 2012 may increase opportunities for US exports.

Executive Summary:

Production:

China's aquatic production in 2012 is forecast at 55.3 MMT, up more than one percent from 2011. The aquaculture sector is expected to continue growing, albeit at a somewhat slower pace. Wild caught production, including overseas sourced, is not expected to rise in the future due to resource restrictions.

Demand:

- Domestic - Rising affluence is driving domestic dietary habits toward alternative protein sources, including aquatic products, and increasing domestic consumption.

- International - Sales to major export markets are rising as world economies rebound.

Total aquatic trade:

- The value is expected to increase rapidly to an estimated $21.7 billion in 2011 from $17.2 billion last year and produce a $10.2 billion surplus.

- China’s exports to the United States climbed to $2.1 billion in the first ten months of 2011.

- Aquatic imports from the United States increased to $930 million in the first ten months of 2011, up 58 per cent over the same period in the previous year.

Challenges:

- Investment in new aquaculture facilities slowing, environmental concerns and coastal development will limit resources available for seawater aquaculture expansion.

- Limited resources restrain growth for wild catch increases.

- Robust processing industry faces rising production costs and labour shortages.

- Increase in international regulations.

Export Opportunities:

- Prospects remain strong for US salmon, frozen fish.

- Reduction in import duties on several fish products in 2012 could boost imports for domestic consumption.

Production

China expected to remain top aquatic producer

China remains the world’s largest aquatic product producer. China’s fishery sector is primarily aquaculture, both fresh and seawater cultures, and accounted for approximately 72 per cent of total aquatic production in 2011. The wild-catch component is significantly smaller and declining wild fishery resources, both domestic and overseas, will contain future potential growth.

Aquaculture is expected to continue growing, albeit at a somewhat slower pace than previous years. In 2011, new aquaculture area increased five per cent over the previous year, a significant drop from a 14 per cent increase in 2009, indicating investment in new facilities may have peaked.

2010 total aquaculture area

Total aquaculture water area reached 7.65 million hectares (MHa) in 2010 from 7.28 MHa in the previous year, with the majority (220,000 HA) of expansion in seawater facilities.

In further developing its coastal water resources, Liaoning Province in northeast China remains the top producer with a 2010 net increase of 128,000 hectare (HA) (compared to a net increase of 266,000 HA in 2009), followed by Shandong and Yunnan with net increases in aquaculture area of 71,000 HA and 32,000 HA in 2010, respectively. MOA officials relate that further expansion of water resources, especially seawater for aquaculture, will face serious challenges from environmental concerns and the rapid industrialization/urbanisation of China’s coastal region. Future production gains may have to incorporate technology and innovation to maintain additional growth.

For 2010, Shandong, Guangdong, and Fujian provinces, due to favorable coastal locations and abundant freshwater resources/facilities, are expected to remain the largest aquatic producers. Hubei, Guangdong, and Jiangsu provinces are the largest in terms of freshwater cultured production.

Aquatic Production expected to increase in 2012

Aquatic production for the first half of 2011 reached 22.8 MMT with a cultured production of 17 MMT, up 2.8 per cent over the same period in 2010, and accounting for 75 per cent of total production, based on China’s Ministry of Agriculture (MOA). 2012 total aquatic production is forecast at 55.3 MMT, compared to an estimated 54.6 MMT in 2011 and 53.7 MMT in 2010. Total wild catch production in 2011 is expected to maintain last year’s level.

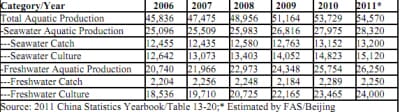

China’s aquatic production (Unit: 1000 Metric Ton)

Total fish production stood at 31.3 MMT in 2010 (up 1.4 MMT from the previous year), accounting for 58 per cent of the total aquatic production, followed by shellfish and crustaceans at 23 and 10 per cent, respectively. Cultured fish continues to dominate with total production of 21.4 MMT, accounting for 68 per cent of total fish production in 2010. Carp remains the most popular cultured freshwater fish with total production of 15.1 MMT in 2010 (from 14.5 MMT in 2008), accounting for 73 per cent of total freshwater cultured fish production.

Tilapia, another popular cultured product, saw 2010 production of 1,332,000 MT, up six percent from 2009, but a drop from the previous ten year average of 11 per cent. Lower prices in 2009 and abnormal weather conditions in 2010 had driven down production. The 2011 tilapia production is expected to resume strong growth in response to foreign market demand and increasing domestic consumption, but the overall rebound will be impacted by increasingly serious disease outbreaks (streptococcicosis) and other factors (see following paragraph – Challenges).Guangdong, Guangxi, Fujian and Hainan continue to be the top four tilapia producers. Yunan province has been developing water resources for tilapia farming with total production approaching 60,000 MT in 2010.

Total catfish production was 591,000 MT in 2010, up from the 558,000 MT in 2009 and is expected to rise in 2011 in response to dynamic domestic consumption. Catfish production for export remains soft in response to uncertainty regarding pending US import policies.

Shellfish, primarily cultured in seawater, continued to show moderate growth with 2010 production of 11.3 MMT (See table), and accounted for 76 per cent of total sea water cultured production.

Cultured crustacean production reached 3.2 MMT in 2010, up 7.5 per cent over the previous year and is expected to remain strong in 2011 in response to domestic demand; catch production remains almost unchanged in 2010. Cultured penaeus vannamei (also known as white shrimp) production exceeded 1.2 MMT (up from the 1.1 MT in 2009), accounting for 38 percent of total cultured crustacean production.

Although there are freshwater aquaculture facilities nationwide, particularly for carp, some species’ production is limited to certain regions due to available resources and climatic conditions. For example, 90 per cent of tilapia production occurs in four provinces, Guangdong, Guangxi, Hainan, and Fujian in 2010. 57 per cent of catfish production is located in Sichuan, Jiangxi, Hubei, Guangdong and Hunan provinces.

The largest producers for both cultured freshwater and seawater shrimp and prawn are Guangdong, Jiangsu, Hubei, Guangxi, Zhejiang and Guangxi provinces. In 2010, Guangdong was the largest shrimp producer with total cultured production of 554,000 MT (compared to the 537,000 MT in 2009), of which Penaeus uannamei production reached 449,900 MT in 2010.

Eel production is concentrated in Fujian, Guangdong, and Jiangxi provinces with much of the production destined for the Japanese market. Shandong, Fujian, Guangdong, and Liaoning provinces dominate the cultured shellfish production accounting for 80 per cent of the 2010 total.

Production Challenge

Tilapia faces disease, competition

According to industry sources, streptococcus disease continued to adversely impact tilapia production in 2011. Experts believe deteriorating water environments and high-density farming has led to high bacteria counts. Low quality inputs, including feed and fingerling stock, and overuse of antibiotics are also contributing to disease conditions. These problems will impact tilapia production and quality in the near future. Another challenge for the tilapia industry is the increased production and exports of Basa fish by Viet Nam.

Industry experts state that Viet Nam’s Basa 40 per cent meat rate (compared to 33 per cent for tilapia) and lower price took significant market share from China’s tilapia sales in the United States in 2011. Industry leaders are studying ways to raise China’s tilapia competiveness in the international market. A new international aquaculture certification system initiated by the World Wildlife Fund (WWF) is also likely to impact China’s tilapia production and exports.

Aquatic catch production is shrinking

Total 2011 catch production of 15.5 MMT is almost unchanged from 2010 and catch production is unlikely to increase in the foreseeable future due to limited availability of resources. Seawater catch production from other territorial seas was 1,116,000 MT in 2010, up from 977,000 MT last year. Industry insiders believe it will be difficult to increase production significantly from other territorial seas.

Further Reading

| - | You can view the full report by clicking here. |