Feed Grains Production Down in 2008, Prices Strong

U.S. feed grain production in 2008 is expected to be down from 2007 because of reduced acreage. The June 30 Acreage report showed planted and harvested area to be down from last year for corn, sorghum, and oats, while that for barley increased from 2007. Slight adjustments were made in feed grain use this month to reflect June 1 stocks. The resulting changes raised 2007/08 ending stocks and 2008/09 supplies, but 2008/09 ending stocks are expected to remain at relatively low levels. Forecast 2008/09 prices for all four feed grains were raised this month as competition from soybeans for 2009 acres is expected to support corn prices in the new marketing year.

Increases in projected world coarse grain use in 2008/09 more than offset larger production prospects this month. Foreign coarse grain ending stocks are projected down enough to offset more than half the increase in U.S. corn stocks.

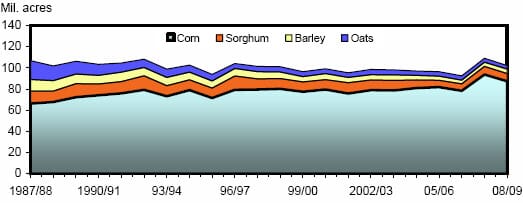

Planted area for U.S. corn, sorghum, barley, and oats

Sources: USDA, National Agricultural Statistics Service, Quick Stats, and USDA, Foreign Agricultural Service, Grain: Word Markets and Trade (Grain Circular).

Domestic Outlook

Feed Grains Supply To Shrink In 2008/09

U.S. feed grain production in 2008 is projected at 314.3 million metric tons, down 713,000 tons from a month ago and down 36.5 million from 2007. The June 30 Acreage report showed planted acres increased from earlier intentions for corn and oats, while sorghum and barley acres declined. The first survey-based production forecast for barley was down 17 million bushels from the previous projection, which was based on trend yields and expected plantings, and oats was up 2.9 million bushels. The U.S. Department of Agriculture (USDA) will make its first survey-based forecasts for corn and sorghum in the August 12 Crop Production report.

Feed grain supply in 2008/09 is projected at 362 million metric tons, up 4 million from last month but down 28.5 million tons from 2007/08. Feed grain imports remain unchanged from last month but are down 477,000 tons from 2007/08. Beginning stocks were increased 4.7 million tons this month to 44.6 million because of lower use in 2007/08.

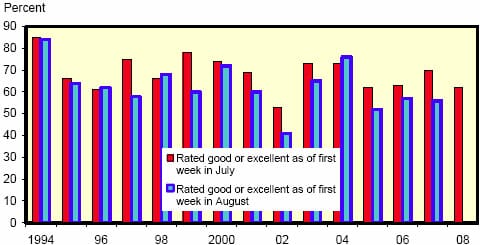

Corn conditions are down so far in 2008

Source: USDA, National Agricultural Statistics Service, Weekly Weather and Crop Bulletin.

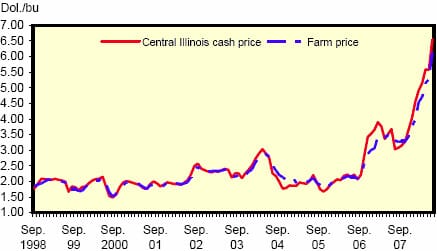

U.S. corn: Central Illinois cash and average farm price, monthly, September 1998-June 2008

Sources: USDA, Agricultural Marketing Service, Weekly Grain Market News Summary, and USDA, Economic Research Service, Feed Grains Database.

Projected total use of feed grains in 2007/08 was decreased 4.5 million tons this month, reflecting lower-than-expected feed and residual use, food and industrial use, and ethanol production. Ending stocks for 2008/09 are projected at 25.2 million tons, up 4.3 million tons from last month but down 19.4 million tons from 2007/08.

2008/09 Corn Production Projected Lower

The projection for 2008 corn production was decreased 20 million bushels from last month because of a reduction in forecast yield. Producers increased plantings 1.3 million acres from their March intentions to 87.3 million acres; however, this is down from 93.6 million acres in 2007. Despite the decrease from 2007, planted acreage is at its second highest level since 1946. Producers planted 80 percent of their acreage with biotech seed varieties, up 7 percent from 2007. Projected yield was lowered 0.5 bushels from last month to 148.4 bushels per acre, due to the decline in the harvested area in the higher yielding Corn Belt States as indicated in the Acreage report. As of July 7, 62 percent of the corn crop was rated good or excellent, down from 70 percent last year.

In addition to the usual uncertainty at this time of year about prospective yields, there is an unusual amount of uncertainty about acreage. This year has had one of the latest planting seasons on record due to heavy rainfall in many areas. At the time of USDA’s National Agricultural Statistics Service's (NASS) acreage survey, conducted in early June, a majority of the flooding had not occurred yet. Although mid-June is typically the cutoff date for corn plantings, many farmers may have continued to plant past this time because of rising prices. NASS resurveyed farmers in six States at the end of June to better determine final plantings. NASS plans to resurvey farmers in the flooded areas in July, and this information will be incorporated in the August survey-based forecast of area, yield, and production.

Projected corn use in 2007/08 is down 165 million bushels from last month’s projection to 12.8 billion bushels. For 2007/08, feed and residual use was decreased 100 million bushels from last month to reflect lower-than-expected third quarter (March-May) disappearance as indicated in the June 30 Grain Stocks report. Exports for 2007/08 remain unchanged this month. Food, seed, and industrial (FSI) use was decreased 65 million bushels because of weaker-than-expected year-to-date use in high fructose corn syrup and starch. FSI is expected to total 4.295 billion bushels, accounting for 34 percent of total use. Ending stocks for 2007/08 were increased 165 million bushels.

For 2008/09, feed and residual use was increased 50 million bushels to 5.2 billion, because of the continued large numbers of livestock and poultry. FSI use of corn is expected to total 5.295 billion bushels, a decrease of 65 million bushels from last month and representing 42 percent of total use. Corn used to produce ethanol was lowered 50 million bushels to 3.95 billion bushels, representing 32 percent of total use. Factors contributing to lower ethanol production were reported delays in plant startups and construction, and lower expected plant capacity utilization as indicated by the most recent ethanol production data. Exports in 2008/09 remained unchanged from last month at 2.0 billion bushels. Forecast ending stocks for 2008/09 are up 160 million bushels, at 833 million.

The projected farm price range for 2008/09 was increased to $5.50-$6.50 per bushel, up 20 cents on each end of the range. Increased competition from soybeans for 2009 acres is expected to support corn prices in the new marketing year. In 2007/08, the season average price received by farmers is expected to be $4.25- $4.45, unchanged from last month.

2008/09 Sorghum Production Projected Higher

Sorghum production in 2008 is projected at 420 million bushels, up 5 million bushels from a month ago because of increased harvested acres. Sorghum plantings are estimated at 7.3 million acres, down 144,000 from the March intentions. Harvested area is forecast at 6.4 million acres, up 110,000 acres from last month’s projection, which was based on March planting intentions and a 4-year average difference between planted and harvested acres, 2004-07. The projected yield is decreased slightly, reflecting rounding in the production projection.

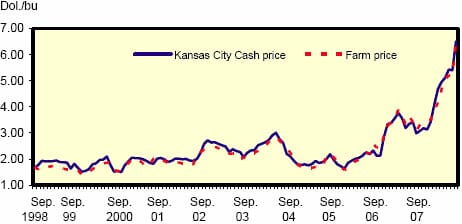

U.S. sorghum: Kansas City cash and average farm price, monthly, September 1998-June 2008

Sources: USDA, Agricultural Marketing Service, Weekly Grain Market News Summary, and USDA, Economic Research Service, Feed Grains Database.

Total supply in 2008/09 is projected to be 482 million bushels, down from 537 million in 2007/08. Total use in 2008/09 is unchanged this month at 420 million bushels. The 2007/08 supply and demand estimates remain unchanged. Ending sorghum stocks for 2008/09 are projected at 62 million bushels, unchanged from a year earlier. The 2008/09 season average sorghum farm price is projected at $5.10-$6.10 per bushel, up from $4.10-$4.30 per bushel in 2007/08.

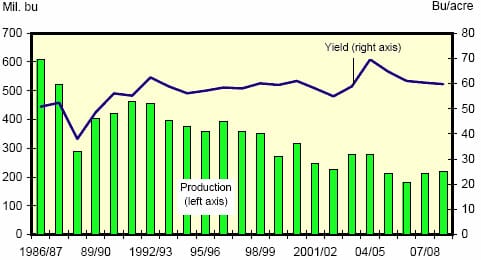

Barley Yield Decreases in 2008/09

The first survey-based forecast of 2008 barley production is 218 million bushels, down 17 million bushels from last month’s projection. Growers seeded 4.13 million acres for 2008, up 3 percent from the 4.02 million acres seeded last year. Harvested acres are at 3.64 million, up 132,000 acres from 2007. Average barley yields are forecast at 59.8 bushels per acre, down from last month’s trend-based projection of 65.5 bushels per acre.

Supply and demand estimates for 2008/09 were unchanged this month. Small changes were made in 2007/08, reflecting the June 1 stocks estimate reported in Grain Stocks, which finished the marketing year for barley. Imports were increased to 30 million bushels from 23 million, due to large barley crop in Canada and preliminary data on Canadian exports. Feed and residual use was increased 1 million bushels to 61 million to keep the data positive. FSI use was decreased to 140 million bushels, down from 145 million last month. FSI data are reported by the Alcohol and Tobacco Tax and Trade Bureau (TTB) and run very late. The most recent data on beer production and barley use are for December 2007. However, feed and residual has never been negative based on actual data from TTB, so FSI was reduced this month. Exports are up 1.4 million bushels to increase to 41.4 million. Ending stocks were reported at 68.2 million bushels, up from the earlier estimate of 58.7 million.

U.S. barley production and yield

Sources: USDA, World Agricultural Outlook Board,WASDE, and USDA, National Agricultural Statistics Service, Quick Stats .

Prices received by farmers for barley in 2008/09 are expected to average $5.80- $6.80 per bushel, compared with $4.02 per bushel in 2007/08.

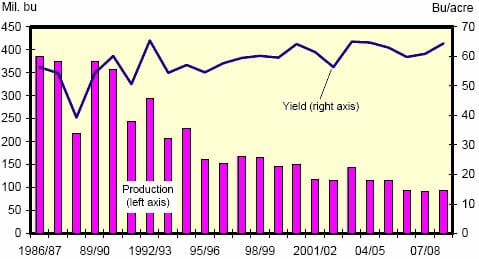

Oats Yield To Increase

Oats production is forecast at 93 million bushels in 2008, according to the first survey results, an increase of 3 million from the previous projection. Planted acreage is up slightly to 3.47 million acres from 3.42 million from the March intentions, but down from the 3.76 million acres planted in 2007. Yields are forecast at 64.4 bushels per acre and are up 3.5 bushels from 2007.

Oats beginning stocks are estimated at 67 million bushels for 2008/09, up 22 million from last month based on the June 1 stocks. These estimates put the total expected 2008/09 oats supply at 265 million bushels, up from 262 million in 2007/08.

For 2007/08, imports were raised 5 million bushels to 120 million from last month, based on preliminary Canadian export data. Feed and residual use was lowered to 118 million bushels, down from 135 million because survey results indicated larger stocks than expected last month. In 2007/08, exports were raised 0.3 million bushels to 2.8 million. Ending stocks were expected at 67 million bushels, up 22 million from last month.

Oats farm prices are projected at $3.80-$4.80 per bushel in 2008/09, compared with $2.63 per bushel in 2007/08.

U.S. oats production and yield

Sources: USDA, World Agricultural Outlook Board,WASDE, and USDA, National Agricultural Statistics Service, Quick Stats.

Harvested Hay Acreage To Decrease in 2008/09

Producers expect to harvest 60.4 million acres of all hay in 2008, down 2 percent from 2007. Expected harvested area of alfalfa and alfalfa mixtures, at 20.8 million acres, is down 4 percent from 2007. Expected area for harvest of all other types of hay totals 39.7 million acres, down 1 percent from the 40.0 million acres harvested in 2007.

Harvested area of all hay is expected to decrease from last year throughout the Great Plains and the West. Increased acres are expected to be harvested along the East Coast. Acreage of alfalfa and alfalfa mixtures decreased in the Corn Belt, the Southeast, and most of the western United States, while acreage increases are expected in the Rocky Mountain States and portions of the Northeast. Lower harvested acreage of other hay is expected in the West Coast, Southwest, and Southern Great Plains portions of the U.S., while increased acreage is expected along the Atlantic Coast, northern Rockies, and northern Great Plains.

Feed and Residual Use To Decline

Feed and residual use of all feed grains in 2008/09 is expected to total 140.6 million metric tons and account for 42 percent of total use. When converted to a September-August marketing year, feed and residual use for the four feed grains plus wheat is projected to total 144.6 million tons, down from 2007/08 forecast of 164.4 million. Corn is estimated to account for 91 percent of the feed and residual use, down from 93 percent in 2007/08. Increased production and feeding of distiller’s spent grains are expected to offset most of this decrease in feed and residual use of the four feed grains plus wheat.

The index of grainconsuming animal units (GCAUs) for 2008/09 is expected to be down 1.31 million units from the 2007/08 forecast of 95.01 million units. The grain used per GCAU would be 1.54 tons, down 11 percent from 2007/08. In the index components, GCAUs for dairy cattle are up slightly, while those for the other categories are down slightly, with cattle on feed being down the most.

Cattle on feed in feedlots with capacity of 1,000 or more head totaled 10.8 million head on June 1, 2008. The inventory was 4 percent below June 1, 2007, and 3 percent below June 1, 2006. Thus, current feed use by cattle in feedlots is expected to decline in 2008. Beef production in 2008 is forecast at 26.7 billion pounds, up from 26.5 billion in 2007 but down from 26.9 billion last month. However, some of the feed needs may be satisfied by increased production of distiller’s spent grains by the expanding ethanol industry.

Pork production in 2009 is expected to decrease 3 percent from the 23.5 billion pounds expected in 2008. Hog farmers responding to the June 2008 survey intend to have 3.07 million sows farrow during the June-August 2008 quarter, down 2 percent from the actual farrowings during the same period in 2007, but up 5 percent from 2006. Intended farrowings for September-November 2008, at 3.05 million sows, are down 4 percent from 2007 but up 3 percent from 2006. As a result, feed use by the pork sector is likely to weaken in 2008/09.

Despite stronger prices, broiler, turkey, and egg production in 2009 is expected to slow from the expected 2008 level, because of the high feed prices. Broiler production in 2009 is expected to decrease 1.1 percent from the projected 2008 production, which is up 2.4 percent from a year earlier. Forecast turkey production in 2009 is down 2.2 percent from 2008, which is up 3.7 percent from 2007. Egg producers are expected to produce 7.6 billion dozen eggs in 2009, up 0.1 percent from the projected 2008 output. These forecast decreases in 2009 production will likely decrease feed use.

Further Reading

| - | You can view the full report by clicking here. |

July 2008